Navigating the world of personal finance can be a daunting task, especially when faced with significant sums of money. One crucial decision involves choosing between structured settlement annuities and traditional investment options. Both offer distinct advantages and drawbacks, requiring careful consideration based on individual financial goals and risk tolerance. This exploration delves into the intricacies of each approach, comparing their potential returns, risks, and suitability for different situations.

Structured settlement annuities, often awarded in legal settlements, provide a guaranteed stream of income over a set period. This can offer stability and predictability, particularly for those seeking financial security and protection against market fluctuations. On the other hand, traditional investment options like stocks, bonds, and real estate, present the potential for higher returns but also carry inherent risks. Understanding the nuances of each approach is essential for making informed decisions that align with individual financial aspirations.

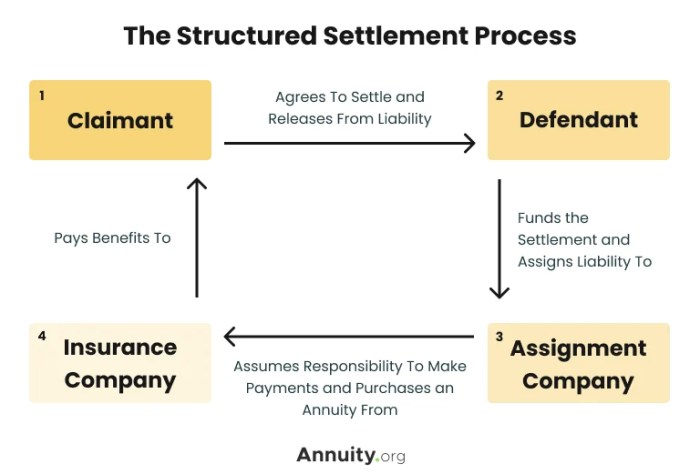

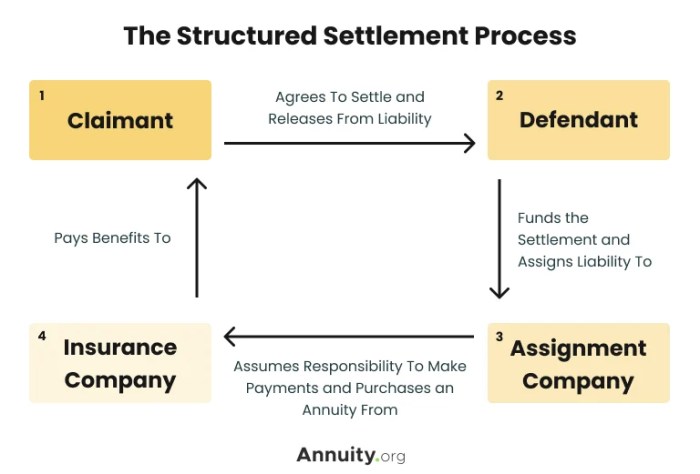

Understanding Structured Settlement Annuities

Structured settlement annuities are a type of financial product designed to provide regular payments over a set period of time. These payments are often used to compensate individuals who have suffered a personal injury or loss, such as in a car accident or medical malpractice case. Unlike traditional lump-sum settlements, structured settlements provide a stream of income, offering a degree of financial security and stability.

Structured Settlement Annuities vs. Lump-Sum Settlements

Structured settlements differ from traditional lump-sum settlements in several key ways. While a lump-sum settlement provides a single, large payment upfront, structured settlements offer regular payments over time. This can be beneficial for individuals who may struggle to manage a large sum of money or who need a steady income stream for future expenses.

- Regular Income Stream: Structured settlements provide a predictable and reliable source of income, which can be crucial for individuals who need financial stability, especially in the aftermath of a significant event.

- Financial Management: Structured settlements can help individuals avoid the potential pitfalls of managing a large lump-sum payment, such as impulsive spending or investment losses.

- Tax Advantages: In many cases, structured settlement payments are tax-free, making them a more advantageous option than a lump-sum settlement, which may be subject to income tax.

- Protection from Creditors: Structured settlement payments are often protected from creditors, ensuring that the funds are available for the intended purpose, such as medical expenses or living costs.

Situations Where Structured Settlements are Used

Structured settlements are typically used in a variety of situations, including:

- Personal Injury Settlements: Structured settlements are commonly used to compensate individuals who have suffered injuries in accidents, such as car accidents, slip-and-falls, or medical malpractice.

- Wrongful Death Settlements: In cases of wrongful death, structured settlements can provide financial support to the surviving family members.

- Product Liability Claims: Structured settlements can be used to compensate individuals who have been injured by defective products.

- Medical Malpractice Cases: In cases of medical negligence, structured settlements can provide financial support for ongoing medical expenses and lost wages.

Benefits of Structured Settlement Annuities

Structured settlement annuities offer a unique approach to managing a lump-sum payment, providing a stream of guaranteed income over time. This can be a highly advantageous option for individuals who require financial stability and long-term security.

Guaranteed Income Stream

Structured settlements offer a guaranteed income stream, which can be crucial for individuals who need reliable financial support for an extended period. This consistent income stream provides peace of mind and ensures financial stability, even in the face of unexpected events.

A structured settlement annuity acts as a financial safety net, providing consistent income payments that can be used to cover essential expenses such as housing, food, healthcare, and education.

Protection Against Inflation and Market Fluctuations

Structured settlements often include provisions for inflation adjustments, which can help to protect the value of the payments over time. This is particularly important in periods of high inflation, as it ensures that the purchasing power of the payments remains relatively stable.

For example, a structured settlement might include a cost-of-living adjustment (COLA) that increases the payments each year based on the rate of inflation. This helps to ensure that the payments maintain their value in real terms.

Financial Stability and Peace of Mind

The guaranteed income stream and protection against inflation provided by structured settlements can offer significant financial stability and peace of mind. Individuals can rely on the regular payments to cover their expenses and avoid the stress of managing investments or dealing with market volatility.

This predictability and stability can be particularly beneficial for individuals with special needs or those who are facing significant medical expenses. It allows them to focus on their health and well-being without worrying about their financial security.

Traditional Investment Options

Traditional investment options offer a wide range of choices for individuals seeking to grow their wealth over time. These options typically involve putting money into assets that have the potential to appreciate in value, providing returns that can be reinvested or withdrawn for various financial goals.

Stocks

Stocks represent ownership in publicly traded companies. When you buy a stock, you become a shareholder and have a claim on the company’s assets and earnings. The value of stocks can fluctuate based on factors like company performance, market sentiment, and overall economic conditions.

- Potential Rewards: Stocks have the potential for high returns, as their value can increase significantly over time, especially for companies that are growing rapidly. They also offer the possibility of receiving dividends, which are payments made by companies to shareholders from their profits.

- Potential Risks: Stocks are volatile investments, meaning their prices can fluctuate significantly in both directions. There is a risk of losing money if the company’s stock price declines or the company goes bankrupt. Market downturns can also impact the value of stocks, potentially leading to significant losses.

Bonds

Bonds are debt securities that represent a loan from an investor to a borrower, typically a government or corporation. When you buy a bond, you are lending money to the borrower in exchange for regular interest payments and the repayment of the principal amount at maturity.

- Potential Rewards: Bonds generally offer lower returns than stocks but are considered less risky. They provide a steady stream of interest payments, and the principal amount is typically repaid at maturity.

- Potential Risks: Bonds carry interest rate risk, meaning their value can decline if interest rates rise. They also carry credit risk, meaning there is a chance the borrower may default on the loan and not repay the principal or interest.

Mutual Funds

Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They offer a convenient way to invest in a wide range of assets without having to buy individual securities.

- Potential Rewards: Mutual funds offer diversification, which can help to reduce risk. They are managed by professional fund managers who select and oversee the investments in the portfolio. They also provide liquidity, allowing investors to buy and sell shares easily.

- Potential Risks: Mutual funds are subject to the same risks as the underlying investments in their portfolios. They also have management fees, which can impact returns.

Real Estate

Real estate refers to land and any structures built on it. Investing in real estate can take many forms, including buying residential or commercial properties, investing in real estate investment trusts (REITs), or participating in real estate crowdfunding.

- Potential Rewards: Real estate can provide rental income, appreciation in value, and tax advantages. It can also serve as a hedge against inflation.

- Potential Risks: Real estate investments can be illiquid, meaning it can be difficult to sell quickly. They are also subject to market fluctuations, economic downturns, and local economic conditions.

Investment Process for Beginners

For those new to investing, it is important to start with a solid understanding of the basics.

- Define Your Financial Goals: Determine your investment goals, such as saving for retirement, buying a home, or funding your children’s education.

- Assess Your Risk Tolerance: Understand your comfort level with risk and potential losses.

- Choose a Brokerage Account: Select a reputable brokerage firm that offers a platform that meets your needs and investment style.

- Start Small and Diversify: Begin with a small amount of money and gradually increase your investment over time. Diversify your portfolio across different asset classes to reduce risk.

- Monitor Your Investments: Regularly review your portfolio and make adjustments as needed to stay on track with your goals.

Comparing Structured Settlements and Traditional Investments

Structured settlements and traditional investments offer different approaches to managing a lump sum of money. Understanding their key differences can help you make an informed decision that aligns with your financial goals and risk tolerance.

Potential Returns and Risks

The potential returns and risks associated with structured settlements and traditional investments differ significantly.

- Structured Settlements: Structured settlements provide a guaranteed stream of payments over time, typically with a fixed interest rate. This offers stability and predictability, ensuring regular income regardless of market fluctuations. However, the fixed interest rate may result in lower returns compared to potentially higher-yielding traditional investments.

- Traditional Investments: Traditional investments, such as stocks, bonds, and real estate, have the potential for higher returns but also carry greater risk. The value of these investments can fluctuate significantly, leading to potential losses.

Factors Influencing the Choice

Several factors influence the decision between structured settlements and traditional investments, including:

- Risk Tolerance: Individuals with a low risk tolerance may prefer the guaranteed income and stability of a structured settlement. Conversely, those willing to take on more risk might favor traditional investments with the potential for higher returns.

- Time Horizon: The time horizon for which the funds are needed is crucial. Structured settlements are suitable for long-term financial planning, as they provide consistent income over an extended period. Traditional investments are more suitable for shorter-term goals where flexibility and potential for growth are desired.

- Financial Goals: The specific financial goals also play a role. If the goal is to secure a steady income stream, a structured settlement may be more appropriate. However, if the goal is to accumulate wealth for a specific purpose, such as retirement or a down payment on a house, traditional investments might be a better choice.

Scenarios for Advantageous Options

Here are some scenarios where one option might be more advantageous than the other:

- Scenario 1: Long-term Income Security: A person who has received a significant settlement due to an injury may prefer a structured settlement to ensure a stable income stream for life. This provides financial security and peace of mind, knowing that regular payments will be received regardless of market conditions.

- Scenario 2: High-Growth Potential: An individual with a longer time horizon and a higher risk tolerance might choose traditional investments to maximize their potential returns. This strategy could be suitable for long-term goals such as retirement planning, where time allows for market fluctuations and potential growth.

Key Considerations for Decision-Making

Choosing between a structured settlement annuity and traditional investment options is a significant financial decision. The best choice depends on your individual circumstances, financial goals, and risk tolerance. It’s essential to consider all factors before making a decision.

Understanding Individual Financial Circumstances and Goals

Your financial situation and objectives play a crucial role in determining the best investment strategy. For example, if you need a steady stream of income for a specific period, a structured settlement annuity might be a suitable option. However, if you have a longer time horizon and are comfortable with potential market fluctuations, traditional investments could be more advantageous.

Seeking Professional Financial Advice

Navigating complex investment decisions can be challenging. Seeking professional financial advice from a qualified advisor can help you make informed choices. An advisor can assess your individual circumstances, goals, and risk tolerance and recommend a suitable investment strategy. They can also provide insights into the intricacies of structured settlement annuities and traditional investment options.

Factors to Consider Before Making a Decision

- Time Horizon: How long do you need the funds? Structured settlement annuities provide guaranteed payments for a fixed period, while traditional investments have the potential for growth over time.

- Risk Tolerance: How comfortable are you with potential market fluctuations? Structured settlement annuities offer a fixed return, while traditional investments carry a higher risk but also the potential for higher returns.

- Tax Implications: Understand the tax implications of both structured settlement annuities and traditional investments. Structured settlements may be subject to income tax, while traditional investments have different tax rules depending on the type of investment.

- Fees and Expenses: Compare the fees associated with structured settlement annuities and traditional investments. Structured settlements may have administrative fees, while traditional investments may have brokerage fees or mutual fund expense ratios.

- Flexibility: Structured settlement annuities provide a fixed stream of income, while traditional investments offer more flexibility in terms of investment choices and withdrawals.

Illustrative Scenarios and Examples

To understand the practical implications of structured settlements versus traditional investments, let’s delve into some illustrative scenarios and examples. These examples will showcase the potential outcomes of each approach and highlight the factors that can influence decision-making.

Potential Outcomes Comparison

To visualize the potential outcomes, consider a hypothetical scenario where an individual receives a $1 million structured settlement or decides to invest that amount in a traditional investment portfolio. Here’s a simplified comparison of the potential outcomes over a 20-year period, assuming different investment scenarios and a 5% annual return for the traditional portfolio:

| Year | Structured Settlement (Annual Payment) | Traditional Investment Portfolio (5% Annual Return) |

|---|---|---|

| 1 | $50,000 | $1,050,000 |

| 5 | $50,000 | $1,276,281 |

| 10 | $50,000 | $1,628,895 |

| 15 | $50,000 | $2,078,928 |

| 20 | $50,000 | $2,653,300 |

It’s important to note that these are simplified examples and actual outcomes can vary significantly based on factors such as investment performance, inflation, and individual circumstances.

Beneficiaries of Structured Settlements

Individuals who may benefit from structured settlements often have specific needs and goals:

- Individuals with a history of financial mismanagement: Structured settlements provide a consistent income stream, reducing the risk of impulsive spending or financial miscalculations.

- Individuals with long-term care needs: Structured settlements can ensure a steady source of income for ongoing medical expenses and care.

- Individuals with limited financial literacy: Structured settlements offer a simplified approach to managing a large sum of money, eliminating the need for complex investment decisions.

Beneficiaries of Traditional Investments

Individuals who may benefit from traditional investments typically have:

- Strong financial literacy and risk tolerance: They can actively manage their investments, seeking higher returns with the understanding of associated risks.

- Long-term financial goals: They are comfortable with the potential for market fluctuations and are willing to invest for the long term.

- A desire for potential growth: They aim to maximize their investment potential and potentially outpace inflation over time.

Decision-Making Flowchart

A flowchart can illustrate the decision-making process for choosing between structured settlements and traditional investments:

[Image of a flowchart illustrating the decision-making process for choosing between structured settlements and traditional investments. The flowchart should include key factors such as financial literacy, risk tolerance, time horizon, and specific needs. It should also include decision points for seeking professional financial advice.]

Ultimately, the decision between structured settlement annuities and traditional investments depends on a myriad of factors, including risk tolerance, time horizon, and financial goals. Seeking professional financial advice is crucial, especially when dealing with significant sums of money. By carefully analyzing individual circumstances and exploring the pros and cons of each option, individuals can make well-informed choices that pave the way for a secure and prosperous future.

Helpful Answers

What are the tax implications of structured settlement annuities?

Structured settlement annuities are generally tax-free, but it’s important to consult with a tax professional to ensure compliance with current regulations.

Can I access the full lump sum of a structured settlement annuity?

Typically, structured settlement annuities are structured as a series of payments, and accessing the full lump sum may be difficult or involve penalties. However, it’s possible to explore options like selling your annuity to a third party.

How do I choose the right investment options for my needs?

Consulting with a financial advisor is recommended. They can help you assess your risk tolerance, time horizon, and financial goals to create a personalized investment plan.