A structured settlement, often awarded in personal injury cases, provides regular payments over time. But what if you need a lump sum of cash now? Selling your structured settlement might be an option, but it’s crucial to understand the process and potential risks involved. This guide will walk you through the steps of selling your structured settlement for a lump sum of cash, from choosing the right broker to navigating the closing process.

From understanding the valuation process to negotiating a fair price, we’ll delve into the complexities of selling your structured settlement. We’ll also explore the potential risks and considerations, helping you make informed decisions about your financial future.

Understanding Structured Settlements

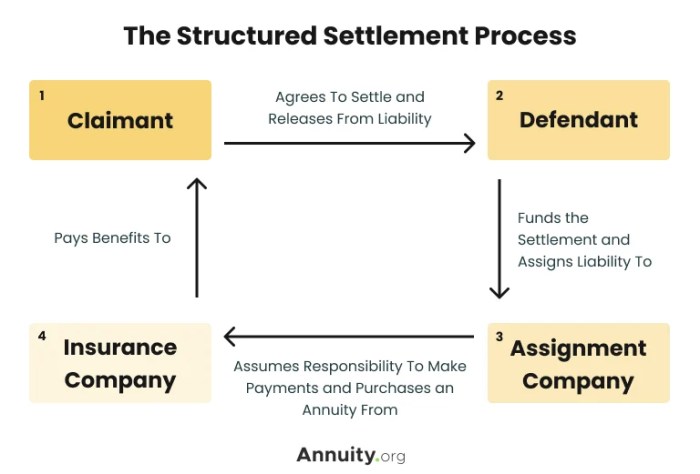

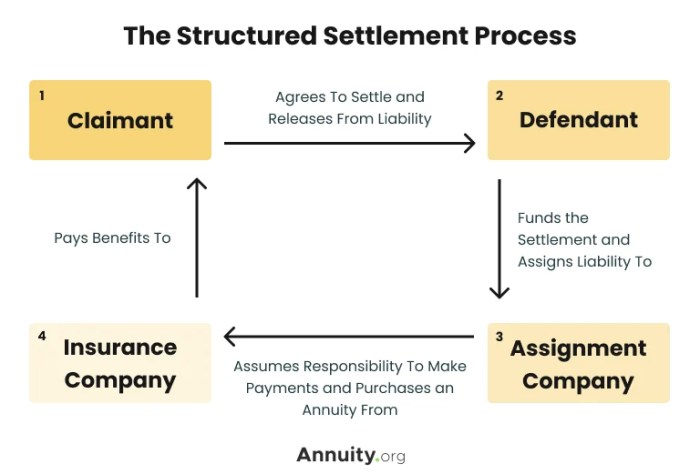

A structured settlement is a legal agreement that provides a person with a stream of regular payments over a set period of time, rather than a lump sum of money. They are often used in personal injury cases, wrongful death cases, and other situations where someone has been injured or has suffered a loss. The purpose of a structured settlement is to ensure that the injured person receives the financial support they need over time, rather than being faced with a large sum of money that they may not know how to manage.

Features of a Structured Settlement

Structured settlements are designed to provide a steady income stream for the recipient. They typically include the following features:

- Periodic Payments: The payments are typically made on a monthly or annual basis, depending on the terms of the agreement.

- Guaranteed Payments: The payments are guaranteed for a specific period of time, such as a number of years or for the recipient’s lifetime.

- Potential Tax Advantages: In some cases, the payments from a structured settlement may be tax-free, or may only be taxed at a lower rate than ordinary income.

Situations Where Structured Settlements Are Used

Structured settlements are often used in the following situations:

- Personal Injury Cases: These settlements are common in cases involving car accidents, medical malpractice, and other types of personal injury.

- Wrongful Death Cases: In wrongful death cases, the settlement provides financial support to the deceased person’s family.

- Other Situations: Structured settlements may also be used in cases involving product liability, discrimination, and other types of legal claims.

Reasons for Selling a Structured Settlement

Sometimes, despite the benefits of receiving regular payments over time, individuals might find themselves needing a lump sum of cash. This is where selling a structured settlement comes into play, offering a way to access the future value of your payments in a single payment. There are various reasons why someone might consider selling their structured settlement.

Common Financial Needs

It’s crucial to understand the various financial situations that might necessitate selling a structured settlement. These needs can range from immediate emergencies to long-term financial planning.

- Unexpected Expenses: Unforeseen events like medical emergencies, home repairs, or unexpected job loss can create a sudden need for a large sum of cash. Selling a structured settlement can provide the necessary funds to address these situations.

- Debt Consolidation: High-interest debt, such as credit card debt or payday loans, can be a significant financial burden. Selling a structured settlement can provide the funds to consolidate these debts into a lower-interest loan, potentially saving money on interest payments.

- Business Opportunities: Starting a business or investing in a promising venture often requires a significant upfront investment. Selling a structured settlement can provide the capital needed to pursue these opportunities.

- Homeownership: Purchasing a home requires a large down payment, and selling a structured settlement can provide the necessary funds to achieve this goal.

- Education Expenses: Funding higher education, whether for oneself or a family member, can be expensive. Selling a structured settlement can help cover tuition, fees, and living expenses.

Choosing a Structured Settlement Broker

Selling a structured settlement can be a complex process, and choosing the right broker is crucial to ensuring you receive a fair and transparent deal. A structured settlement broker acts as an intermediary between you and potential buyers, helping you navigate the process and obtain the best possible offer.

Factors to Consider When Selecting a Structured Settlement Broker

When choosing a structured settlement broker, several factors should be considered to ensure you select a reputable and reliable professional.

- Experience and Expertise: Choose a broker with a proven track record in structured settlement transactions. Look for brokers with extensive experience in evaluating settlements, negotiating deals, and handling the legal aspects of the transaction.

- Reputation and Licensing: Verify the broker’s reputation by checking online reviews, industry associations, and licensing information. Ensure they are licensed and regulated in your state, adhering to ethical standards and industry regulations.

- Transparency and Communication: A reputable broker will be transparent about their fees and the entire process. They should provide clear and concise information, promptly answer your questions, and keep you informed throughout the transaction.

- Market Knowledge: Brokers should have a deep understanding of the current market conditions for structured settlements. They should be able to provide accurate estimates of the fair market value of your settlement and advise you on the best options available.

- Client Testimonials and References: Request client testimonials and references to gain insights into the broker’s track record and client satisfaction. Contact previous clients to gather firsthand information about their experience.

- Fees and Payment Structure: Understand the broker’s fees and payment structure. Look for brokers who offer competitive rates and transparent fee schedules. Be wary of brokers who charge upfront fees or have hidden charges.

Comparing Broker Services

Different brokers may offer varying services, so it’s essential to compare their offerings to find the best fit for your needs.

- Valuation Services: Some brokers provide free or discounted valuations of your structured settlement. They can assess the present value of your future payments and provide an estimated range of offers you might receive.

- Legal Expertise: Some brokers have in-house legal expertise or collaborate with experienced attorneys specializing in structured settlement transactions. This can be beneficial for navigating legal complexities and ensuring compliance with regulations.

- Negotiation Skills: Experienced brokers are skilled negotiators who can leverage their market knowledge and expertise to secure favorable terms for you. They can negotiate the purchase price, payment terms, and other relevant aspects of the transaction.

- Customer Support: Choose a broker who offers excellent customer support and is readily available to answer your questions and address your concerns. They should be responsive and proactive throughout the process.

Verifying Broker Credentials and Reputation

Verifying a broker’s credentials and reputation is crucial to ensure you’re dealing with a legitimate and trustworthy professional.

- Licensing and Regulation: Check if the broker is licensed and regulated in your state. You can contact your state’s Department of Insurance or a similar regulatory agency to verify their credentials.

- Industry Associations: Look for membership in reputable industry associations, such as the National Association of Settlement Purchasers (NASP). Membership in these associations often indicates adherence to ethical standards and industry best practices.

- Online Reviews and Testimonials: Read online reviews and testimonials from previous clients to get an understanding of the broker’s reputation and client satisfaction. Look for reviews on websites like Trustpilot, Yelp, and Google Reviews.

- Better Business Bureau (BBB): Check the broker’s rating with the Better Business Bureau (BBB). The BBB provides information about businesses and their history, including any complaints or customer reviews.

Understanding the Valuation Process

Determining the fair market value of your structured settlement is a crucial step in the selling process. Structured settlement brokers use a variety of methods to arrive at a fair price, taking into account several factors that influence the value of your payments.

Factors Influencing Valuation

The valuation process considers several key factors that impact the present value of your future payments. These factors include:

- Interest Rates: Interest rates play a significant role in determining the present value of future payments. Lower interest rates result in a higher present value, as the money can grow more slowly over time. Conversely, higher interest rates result in a lower present value, as the money can grow faster over time.

- Future Payments: The amount and frequency of your future payments directly influence the valuation. Larger payments and more frequent payments generally result in a higher present value.

- Time Value of Money: The time value of money is a fundamental principle in finance, which states that money today is worth more than the same amount of money in the future. This is because money can earn interest over time, making it more valuable today.

- Discount Rate: The discount rate is a rate used to calculate the present value of future payments. This rate takes into account the time value of money, inflation, and other factors that affect the value of money over time.

- Risk Assessment: The broker will assess the risk associated with your structured settlement. This may include factors like your age, health, and the likelihood of receiving all future payments.

Potential Risks of Overvaluation or Undervaluation

- Overvaluation: An overvalued structured settlement could result in you receiving less cash than you deserve. This can happen if the broker uses unrealistic assumptions or does not accurately assess the risk associated with your settlement.

- Undervaluation: An undervalued structured settlement could result in you receiving less cash than you could have. This can happen if the broker does not adequately consider the factors that influence the present value of your future payments.

Negotiating the Sale

Once you’ve chosen a structured settlement broker, it’s time to negotiate the sale of your structured settlement. This involves finding the best possible deal that balances your financial needs with the broker’s profit margin.The negotiation process involves several steps, including understanding the valuation process, exploring different payment options, and considering the legal implications of the sale.

Negotiating the Sale Price

It’s crucial to understand the factors influencing the sale price of your structured settlement. These factors include the total value of the settlement, the remaining payment schedule, the interest rate, and the current market conditions. Negotiating a fair price involves understanding the valuation process and exploring different payment options. Here are some tips for negotiating the sale price:

- Research Comparable Sales: Before negotiating, research comparable sales of structured settlements. This will give you an idea of what other sellers have received for similar settlements.

- Consider Different Payment Options: Explore different payment options with your broker, such as lump-sum payments, installment payments, or a combination of both. This flexibility can help you achieve a more favorable price.

- Be Prepared to Walk Away: If you’re not satisfied with the broker’s offer, be prepared to walk away. This shows that you’re serious about getting a fair deal.

- Don’t Rush the Process: Take your time negotiating and don’t feel pressured to accept the first offer. It’s best to thoroughly understand the terms of the agreement before signing any documents.

Legal Implications of the Sale

It’s important to understand the legal implications of selling your structured settlement.

Selling your structured settlement is a legally binding transaction.

You should consult with an attorney to ensure that you fully understand the terms of the agreement and the potential tax consequences of the sale. The legal process includes:

- Court Approval: In most cases, the sale of a structured settlement requires court approval. This ensures that the transaction is fair and protects the interests of all parties involved.

- Legal Counsel: It’s essential to consult with an attorney specializing in structured settlement transactions. They can guide you through the legal process, review the agreement, and ensure that your rights are protected.

Closing the Transaction

Once you have negotiated the terms of the sale with a structured settlement broker, the final step is closing the transaction. This involves a series of steps to ensure all parties involved are protected and the process is conducted legally and transparently.

Documentation Required for Closing

The closing process involves a significant amount of documentation to ensure all parties understand the terms of the agreement and that the transaction is executed correctly. The specific documentation required may vary depending on the state and the terms of the sale. However, common documents include:

- Structured Settlement Agreement: This is the primary document that Artikels the terms of the sale, including the purchase price, payment schedule, and any applicable fees.

- Assignment of Structured Settlement Rights: This document legally transfers your rights to the structured settlement payments to the buyer.

- Affidavit of Truthfulness: This document affirms that the information you provided regarding the structured settlement is accurate and complete.

- Release of Claims: This document releases the original settlement payer from any further liability related to the structured settlement.

- Proof of Identity: You will need to provide documentation verifying your identity, such as a driver’s license or passport.

- Financial Disclosure Statements: You may be required to provide financial information to the broker, such as bank statements or tax returns.

Role of Legal Counsel in Closing

It is highly recommended to have legal counsel review all documentation before closing the transaction. A lawyer can ensure that the agreement is fair and protects your interests. They can also advise you on any potential tax implications of the sale.

Potential Risks and Considerations

Selling your structured settlement for a lump sum of cash can be a beneficial decision for some, but it’s crucial to understand the potential risks and downsides before making a choice. This section will delve into these aspects, offering advice on mitigating risks and ensuring a smooth transaction.

Potential Risks

It’s important to be aware of the potential risks associated with selling your structured settlement. While receiving a lump sum can seem attractive, it’s crucial to weigh the pros and cons carefully.

- Loss of Future Payments: By selling your structured settlement, you forfeit future payments, which could potentially be a significant financial loss in the long run. This is especially true if your payments are designed to cover long-term needs like medical expenses or income replacement.

- Lower Lump Sum Than Expected: The actual lump sum you receive may be less than you anticipate. This can occur due to factors like the discount rate used by the buyer, the age and health of the recipient, and the remaining payment term.

- Potential for Fraud: Unfortunately, the structured settlement industry has seen instances of fraud. It’s essential to choose a reputable broker and thoroughly research their track record and legitimacy.

- Tax Implications: Selling your structured settlement may have tax implications. You may need to pay taxes on the lump sum received, potentially reducing the net amount you gain.

- Financial Mismanagement: Receiving a lump sum can be tempting, but it’s crucial to have a plan for managing the funds wisely. If the money is not managed responsibly, it could be quickly spent, leaving you in a worse financial position than before.

Mitigating Potential Risks

While there are risks associated with selling your structured settlement, you can take steps to mitigate them:

- Consult with a Financial Advisor: Before making any decisions, consult with a qualified financial advisor. They can help you assess your financial situation, understand the potential risks and benefits, and create a plan for managing the lump sum if you choose to sell.

- Shop Around for the Best Offer: Don’t settle for the first offer you receive. Get quotes from multiple brokers to compare their rates and terms.

- Understand the Valuation Process: Ensure you understand how the lump sum is calculated and the factors that influence the valuation.

- Thoroughly Review the Contract: Before signing any agreements, carefully review the contract with a lawyer or financial advisor to understand the terms and conditions.

- Consider Alternative Solutions: Explore other options, such as borrowing against your structured settlement, before deciding to sell.

Alternative Solutions to Selling

Instead of selling your structured settlement, you may consider alternative solutions that could provide you with immediate cash while preserving future payments:

- Structured Settlement Loan: This allows you to borrow against your future payments without selling the entire settlement. The loan is repaid over time, usually through a portion of your future payments.

- Structured Settlement Factoring: This involves selling a portion of your future payments for a lump sum. It can be a good option if you need a smaller amount of cash and want to keep receiving the majority of your future payments.

Selling your structured settlement for a lump sum can be a complex decision, but with careful planning and understanding of the process, you can navigate this path successfully. Remember to choose a reputable broker, thoroughly understand the valuation process, and negotiate a fair price. By taking these steps, you can maximize your financial gains and ensure a smooth transaction.

Expert Answers

How much can I expect to receive for my structured settlement?

The amount you receive will depend on various factors, including the remaining payments, interest rates, and the broker’s valuation. It’s best to consult with a broker for a personalized estimate.

Are there any tax implications when selling my structured settlement?

Yes, selling your structured settlement is generally considered a taxable event. Consult with a tax professional to understand the specific tax implications in your situation.

Is it safe to sell my structured settlement?

Working with a reputable broker and understanding the process can help mitigate risks. However, selling your structured settlement does involve potential downsides, so careful consideration is essential.