A structured settlement offers a lifeline for individuals facing significant financial challenges, providing a stream of payments over time. However, the allure of immediate cash can be tempting, leading some to consider selling their structured settlement before its maturity date. This decision, while seemingly advantageous in the short term, can have far-reaching consequences, potentially jeopardizing long-term financial security.

Understanding the intricacies of structured settlements, the potential pitfalls of early sale, and the available alternatives is crucial to making informed financial decisions. This guide delves into the risks associated with selling your structured settlement before maturity, exploring the financial implications, legal considerations, and ethical concerns involved. It also sheds light on alternative solutions for accessing funds from your settlement, empowering you to make the best choice for your unique circumstances.

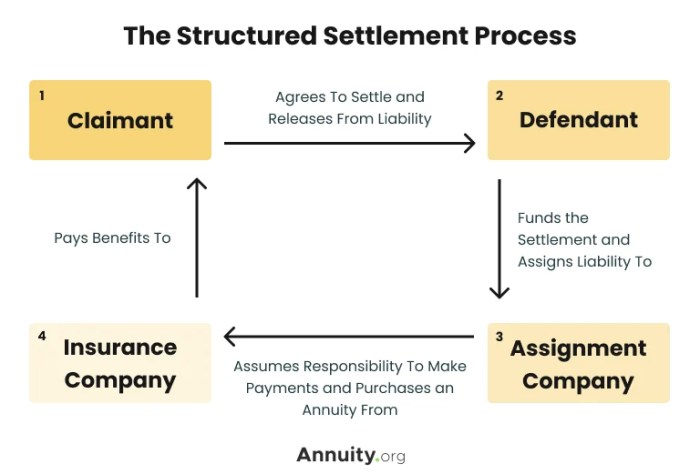

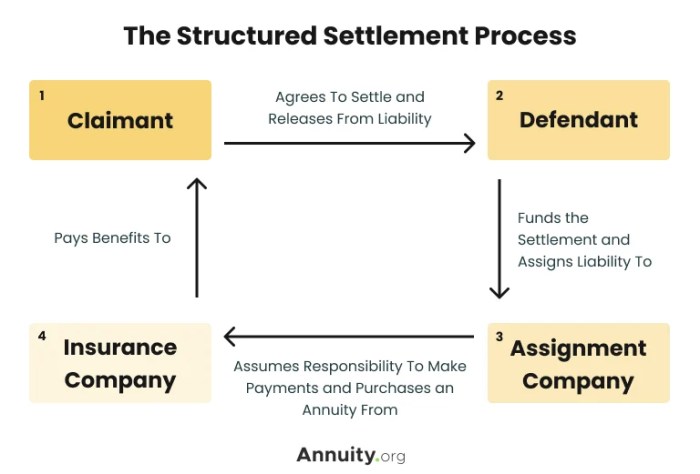

Understanding Structured Settlements

Structured settlements are a unique form of financial compensation often awarded in personal injury cases. They provide a series of payments over time, rather than a lump sum, to ensure the injured party has ongoing financial support for their recovery and long-term needs.

Purpose of Structured Settlements

Structured settlements are designed to provide long-term financial security for individuals who have suffered significant injuries. They offer several benefits compared to lump sum payments:

- Protection from Financial Mismanagement: By receiving regular payments, the recipient is less likely to spend the entire settlement quickly, ensuring funds are available for ongoing medical expenses, rehabilitation, and living costs.

- Tax Advantages: In many cases, structured settlement payments are tax-free, which can significantly reduce the overall tax burden for the recipient.

- Long-Term Financial Stability: Regular payments provide a steady stream of income, helping the injured party maintain financial stability and avoid the risk of running out of funds.

Structure of a Structured Settlement Payment Schedule

Structured settlement payments are typically structured as a series of periodic payments, often monthly or annually, over a predetermined period. The specific payment schedule can vary depending on the circumstances of the case and the needs of the recipient.

- Initial Payment: A lump sum payment may be made at the beginning of the settlement to cover immediate expenses.

- Periodic Payments: Subsequent payments are made at regular intervals, often increasing over time to account for inflation and potential future needs.

- Duration: The duration of the settlement can range from a few years to a lifetime, depending on the severity of the injury and the anticipated needs of the recipient.

Situations Where Structured Settlements are Awarded

Structured settlements are commonly awarded in cases involving:

- Severe Personal Injuries: Individuals who have sustained catastrophic injuries, such as spinal cord injuries, traumatic brain injuries, or severe burns, may be awarded structured settlements to cover ongoing medical expenses, rehabilitation, and lost wages.

- Wrongful Death: Families of victims who have lost loved ones due to negligence or wrongful acts may receive structured settlements to provide financial support for surviving family members.

- Medical Malpractice: Patients who have suffered serious injuries due to medical negligence may be awarded structured settlements to cover medical costs, lost income, and pain and suffering.

“Structured settlements are a powerful tool for ensuring the long-term financial security of individuals who have suffered significant injuries.”

Risks of Selling a Structured Settlement

Selling your structured settlement before maturity can have significant financial implications. While it may seem like a quick solution to immediate financial needs, it’s crucial to understand the potential risks involved.

Potential for Loss of Future Payments

Selling your structured settlement means giving up the right to receive future payments. This can have a substantial impact on your long-term financial security, especially if you need the payments for essential expenses like housing, healthcare, or retirement. For example, consider someone who receives $5,000 per year for the next 20 years. If they sell the settlement for a lump sum, they may only receive $50,000.

If they need the payments for their living expenses, they could be left without income after the lump sum is spent.

The Concept of Present Value

Settlement buyers offer a discounted amount for your structured settlement because they are purchasing the right to receive future payments. This discount is based on the concept of present value, which calculates the current worth of a future payment stream. The discount rate used by settlement buyers is typically higher than the discount rate used by banks and other financial institutions, resulting in a lower lump sum payment for you.

The present value (PV) of a future payment stream is calculated by discounting each future payment to its present value using a discount rate. The formula for present value is:PV = FV / (1 + r)^nWhere:

- PV = Present Value

- FV = Future Value

- r = Discount Rate

- n = Number of Periods

For example, a structured settlement that pays $10,000 per year for the next 10 years might be valued at $67,101 today if the discount rate is 5%. However, a settlement buyer might offer a discount rate of 10%, resulting in a present value of only $53,345. This difference in discount rates can significantly impact the lump sum payment you receive.

Alternatives to Selling

Selling your structured settlement may seem like the only option to access funds quickly, but there are other alternatives you can explore. These alternatives might offer more favorable terms and protect your long-term financial security.Exploring these alternatives can help you make a more informed decision about how to best manage your structured settlement.

Structured Settlement Loans

Structured settlement loans are a popular alternative to selling your structured settlement. They allow you to borrow against the future payments of your settlement without relinquishing ownership.Here are some key points about structured settlement loans:

- You retain ownership of your settlement: Unlike selling, you maintain control over your structured settlement payments.

- Flexible repayment options: You can choose a repayment term that aligns with your financial situation.

- Potentially lower interest rates: Interest rates for structured settlement loans are generally lower than those offered by traditional lenders.

- No impact on your credit score: These loans typically don’t require a credit check, so they won’t affect your credit score.

However, it’s important to note that structured settlement loans come with their own set of considerations:

- Fees and interest: You’ll need to pay back the loan principal and interest, which can add up over time.

- Loan approval process: The approval process for a structured settlement loan may take some time.

- Potential for higher costs: If you default on your loan, you could face penalties and the loss of your structured settlement.

It’s crucial to compare different loan options from reputable lenders and carefully review the terms before committing.

Refinancing a Structured Settlement

Refinancing your structured settlement involves restructuring the payment schedule to receive a lump sum payment or adjust the payment amounts. This option can be advantageous if you need a larger upfront payment or want to increase the amount of your monthly payments.Here’s what you need to know about refinancing:

- Potentially lower monthly payments: Refinancing can help reduce your monthly payments, freeing up cash flow.

- Access to a lump sum: You can receive a lump sum payment upfront, providing immediate access to funds.

- Tailored payment plans: Refinancing allows you to customize your payment schedule to meet your specific needs.

However, refinancing also comes with potential drawbacks:

- Fees and interest: Refinancing involves fees and interest, which can increase the overall cost of your settlement.

- Potential for higher future payments: While you may receive a larger upfront payment, your future payments could be higher.

- Complexity of the process: Refinancing a structured settlement can be a complex process that requires careful consideration.

Legal and Ethical Considerations

Selling a structured settlement involves a complex legal framework and raises important ethical considerations. Understanding these aspects is crucial for both the seller and the buyer, as they impact the transaction’s legitimacy and fairness.

Legal Framework for Structured Settlement Transactions

The legal framework surrounding structured settlement transactions aims to protect the interests of the recipient and ensure that the transfer is conducted fairly and transparently. The process involves multiple legal and regulatory safeguards, including:

- Court Approval: In most cases, the transfer of a structured settlement requires court approval. This ensures that the recipient understands the implications of selling their settlement and that the transaction is fair and in their best interests.

- State Laws: Each state has specific laws governing structured settlement transfers. These laws typically Artikel the procedures for court approval, the types of transactions allowed, and the disclosures required to the recipient.

- Federal Regulations: The federal government also plays a role in regulating structured settlement transactions. The Structured Settlement Protection Act (SSPA), for instance, sets standards for disclosure and requires the involvement of a qualified professional, such as a structured settlement broker or attorney, to represent the recipient’s interests.

Role of the Court in Approving Settlement Transfers

The court plays a vital role in ensuring the fairness and legitimacy of structured settlement transfers. Here’s how:

- Reviewing the Transaction: The court reviews the proposed transfer agreement to ensure that it is fair to the recipient and meets the requirements of applicable state laws. This includes examining the purchase price offered, the fees charged by intermediaries, and the potential risks and benefits for the recipient.

- Protecting the Recipient: The court acts as a guardian for the recipient, ensuring they understand the implications of selling their settlement and are not being taken advantage of. The court may require the recipient to be represented by an independent attorney to protect their interests.

- Hearing and Decision: The court conducts a hearing to gather information and consider the arguments presented by all parties involved. Based on the evidence and legal arguments, the court makes a decision on whether to approve or reject the transfer.

Ethical Considerations in Structured Settlement Transactions

While legal frameworks are in place to regulate these transactions, ethical concerns remain. These concerns stem from the potential for exploitation of individuals who may be vulnerable or desperate for immediate cash.

- Exploitation of Vulnerable Individuals: Individuals who are struggling financially or lack financial literacy may be more susceptible to being taken advantage of by unscrupulous buyers or brokers who offer them low prices for their settlements. This raises ethical concerns about the fairness and transparency of the transaction.

- Lack of Financial Planning: Selling a structured settlement often represents a significant financial decision. Individuals may not have access to proper financial advice or may not fully understand the long-term consequences of selling their future income stream. This raises concerns about the potential for financial hardship and regret later on.

- Pressure Tactics: Some buyers or brokers may use aggressive sales tactics or pressure individuals into selling their settlements, even when it may not be in their best interests. This unethical behavior can lead to individuals making rash decisions they later regret.

Considerations for Decision Making

Selling your structured settlement is a significant financial decision that should not be taken lightly. Carefully weighing the potential benefits against the risks is crucial to ensure you make the best choice for your long-term financial well-being. This section will guide you through various factors to consider when deciding whether to sell your structured settlement. We will examine the pros and cons of selling versus other options, and provide a checklist of questions to ask yourself before making a final decision.

Factors to Consider

- Financial Needs: Determine if you have an immediate financial need that outweighs the long-term benefits of receiving regular payments. Consider the severity and urgency of your financial situation.

- Future Financial Planning: Evaluate how selling your structured settlement will impact your long-term financial goals, such as retirement planning, education expenses, or major purchases.

- Investment Opportunities: Analyze if you have access to investment opportunities that could potentially yield higher returns than the structured settlement payments. Consider the risk tolerance and investment expertise you possess.

- Interest Rates and Inflation: Assess the potential impact of interest rate changes and inflation on the present value of your structured settlement payments. Consider how these factors might affect your overall financial position.

- Tax Implications: Understand the tax implications of selling your structured settlement. Consult with a tax advisor to determine the tax consequences of receiving a lump-sum payment.

- Legal and Ethical Considerations: Be aware of the legal and ethical considerations involved in selling your structured settlement. Ensure you are working with a reputable and licensed company that adheres to all applicable regulations.

Comparison of Selling vs. Other Options

| Factor | Selling Structured Settlement | Other Options |

|---|---|---|

| Immediate Cash | Yes | No |

| Long-Term Financial Security | Potentially Reduced | Potentially Enhanced |

| Flexibility and Control | High | Limited |

| Potential Investment Growth | Depends on Investment Strategy | Potentially Higher |

| Tax Implications | Potentially Higher | Potentially Lower |

| Legal and Ethical Risks | Higher | Lower |

Questions to Ask Yourself

- What are my immediate and long-term financial goals?

- Do I have a clear understanding of the risks and potential consequences of selling my structured settlement?

- Have I explored all alternative options, such as borrowing against the settlement, seeking financial counseling, or negotiating a payment schedule with the settlement provider?

- Have I consulted with a qualified financial advisor, tax advisor, and attorney to understand the full implications of selling my structured settlement?

- Am I confident in my ability to manage the lump-sum payment responsibly and make sound investment decisions?

Navigating the complexities of structured settlements requires careful consideration and a clear understanding of the risks involved. While selling your settlement might appear appealing for immediate financial relief, it’s essential to weigh the potential long-term consequences. By exploring alternative options, seeking professional advice, and thoroughly evaluating your financial needs, you can make an informed decision that safeguards your financial well-being and ensures your future security.

Clarifying Questions

What is a structured settlement?

A structured settlement is a legal agreement that provides regular payments to an individual over a set period of time, often as a result of a personal injury or wrongful death lawsuit.

Why would someone sell their structured settlement?

Individuals might sell their structured settlement for various reasons, such as immediate financial needs, debt consolidation, or investment opportunities.

What are the common risks associated with selling a structured settlement?

The most significant risks include losing future payments, receiving a discounted lump sum, and potential legal complications.

How can I find a reputable structured settlement buyer?

It’s crucial to research and select a reputable buyer with a proven track record and positive customer reviews.

What are some alternatives to selling my structured settlement?

Alternatives include obtaining a structured settlement loan or refinancing your settlement.