Navigating the aftermath of a life-altering event often involves navigating complex financial decisions. One such decision is choosing between a lump sum payment and a structured settlement. While a lump sum might seem appealing for its immediate financial freedom, structured settlements offer a unique set of advantages that can provide long-term financial security and peace of mind.

Structured settlements provide a steady stream of income over time, often with tax benefits and legal protections that can safeguard your financial future. They are particularly advantageous for individuals with ongoing medical expenses or a need for long-term financial stability.

Understanding Structured Settlements

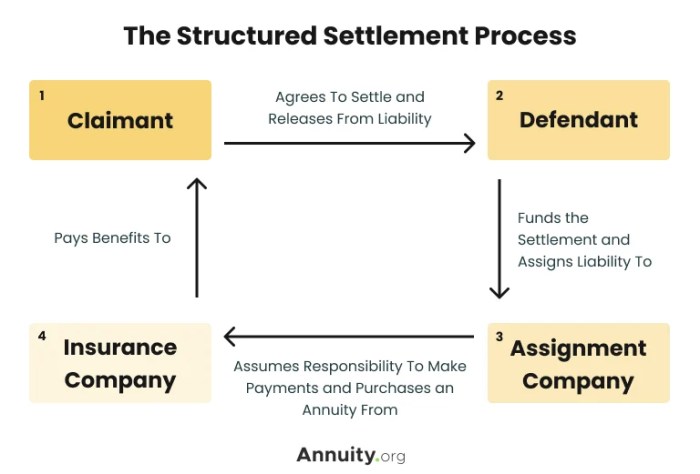

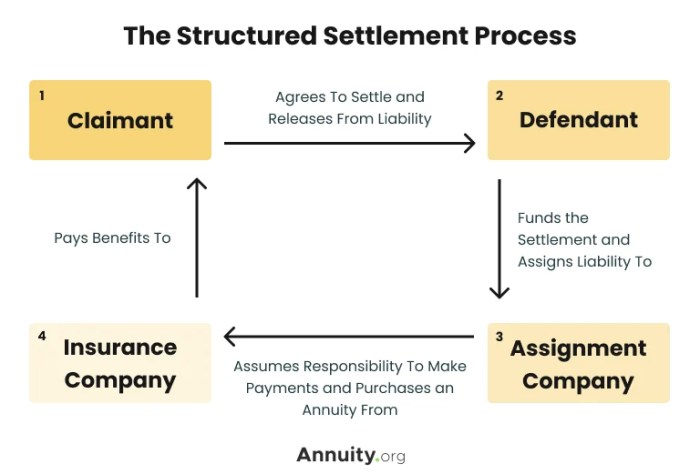

A structured settlement is a legal agreement that provides a person who has suffered a personal injury or wrongful death with a stream of payments over time instead of a lump sum. This structure can be advantageous for individuals seeking financial security and long-term stability.

Types of Structured Settlements

Structured settlements can be tailored to meet the specific needs of the recipient, offering flexibility in payment schedules and options. Here are some common types:

- Periodic Payments: This is the most common type, where the recipient receives regular payments, often monthly or annually, for a predetermined period. This provides a consistent income stream, helping manage finances and plan for the future.

- Lump Sum Options: While structured settlements are primarily focused on long-term financial security, some arrangements allow for a portion of the settlement to be received as a lump sum. This can be beneficial for immediate needs or specific expenses.

- Combinations: Structured settlements can also incorporate a combination of periodic payments and lump sum options, providing flexibility to address both immediate and long-term financial requirements.

Scenarios Where Structured Settlements Are Suitable

Structured settlements can be particularly advantageous in various situations:

- Long-Term Medical Expenses: When a personal injury results in ongoing medical care, a structured settlement can ensure that funds are available to cover these expenses over time. This can provide peace of mind and financial stability for the recipient.

- Disability and Lost Income: In cases of permanent disability, structured settlements can provide a steady income stream to replace lost earnings and maintain a reasonable standard of living. This is particularly important when the individual is unable to return to work.

- Future Expenses: Structured settlements can also be designed to address future expenses, such as education for children or long-term care needs. This ensures that the recipient’s financial needs are met over the long term.

- Protecting Against Financial Mismanagement: Structured settlements can help protect individuals from financial mismanagement, particularly those who may have difficulty managing large sums of money. The regular payments provide a structured approach to financial planning, reducing the risk of impulsive spending or financial instability.

Financial Security and Stability

A structured settlement can offer greater financial security and stability compared to a lump sum payment. This is because it provides a steady stream of income over time, helping you manage expenses and avoid financial strain.

Long-Term Financial Stability

A structured settlement provides a predictable income stream for a predetermined period. This helps you budget effectively and avoid the risk of running out of money. Unlike a lump sum payment, which can be spent quickly, a structured settlement ensures a steady flow of funds for years to come.

Managing Expenses and Avoiding Financial Strain

Structured settlements are particularly beneficial for individuals with ongoing medical expenses. The regular payments can help cover medical bills, living expenses, and other necessities, providing peace of mind and reducing financial stress.

Potential Benefits for Individuals with Ongoing Medical Expenses

- Guaranteed Income: A structured settlement guarantees a consistent income stream, ensuring that you have the financial resources to cover ongoing medical expenses, regardless of unforeseen circumstances.

- Protection Against Inflation: Some structured settlements include provisions for inflation protection, ensuring that your payments keep pace with rising costs of living and medical care.

- Professional Management: Structured settlements are typically managed by a reputable third-party administrator, who handles all aspects of the payments, including tax implications and disbursement. This relieves you of the burden of managing large sums of money and ensures that payments are made on time and as agreed upon.

Protection from Financial Mismanagement

Receiving a large lump sum payment can be overwhelming and tempting, but it also presents significant financial risks. The sudden influx of cash can lead to impulsive spending, poor investment decisions, and even financial ruin. A structured settlement provides a safeguard against these pitfalls by distributing the funds in regular installments over a predetermined period. This structured approach eliminates the temptation to spend the entire amount at once and promotes responsible financial planning.

The Role of a Structured Settlement Trustee

A structured settlement trustee is a crucial element in protecting your financial well-being. The trustee is a neutral third party appointed to manage the funds and ensure they are used for their intended purpose. The trustee’s responsibilities include:

- Safeguarding the settlement funds.

- Disbursing payments according to the terms of the settlement agreement.

- Monitoring the beneficiary’s financial needs and providing guidance.

- Preventing misuse or depletion of the funds.

The trustee acts as a financial guardian, protecting the beneficiary from potential financial mismanagement and ensuring the funds are used responsibly over time. This oversight provides peace of mind, knowing that the settlement funds are being handled prudently and will provide long-term financial security.

Tax Advantages

A structured settlement can offer significant tax advantages compared to a lump-sum payment. Understanding these benefits can help you make an informed decision about the best way to receive your compensation.Structured settlements are generally designed to be tax-friendly. This is because the payments you receive are typically considered to be “structured annuity payments,” which are often tax-free or taxed at a lower rate than lump-sum payments.

Tax-Free Payments

Structured settlements can offer tax-free payments, which can significantly increase the overall financial benefit. This is because you won’t have to pay any taxes on the money you receive.

For example, if you receive a structured settlement of $100,000 over 10 years, and the payments are tax-free, you’ll receive the full $100,000 without having to pay any taxes. If you had received a lump-sum payment of $100,000, you would have had to pay taxes on that amount, which could have reduced your net income significantly.

Lower Tax Rates

In some cases, the payments from a structured settlement may be taxed at a lower rate than a lump-sum payment. This is because the payments are often considered to be “ordinary income,” which is taxed at a lower rate than capital gains.

For example, if you receive a structured settlement of $100,000 over 10 years, and the payments are taxed at a lower rate than a lump-sum payment, you’ll pay less in taxes overall. This can significantly increase the amount of money you have available to spend or save.

Legal and Regulatory Considerations

Structured settlements are governed by a comprehensive legal framework that ensures their fairness, transparency, and protection for both recipients and the parties involved. This framework involves courts, regulatory bodies, and specific legal requirements that safeguard the rights and interests of all parties.

Legal Framework and Regulatory Oversight

Structured settlements are subject to both federal and state laws, ensuring they are established and managed according to specific legal principles. The primary federal law governing structured settlements is the Structured Settlement Protection Act (SSPA), enacted in 1998. The SSPA regulates the transfer of structured settlement payments, providing safeguards against fraudulent or unfair transactions. This law also establishes procedures for the transfer of structured settlement payments, ensuring that recipients are fully informed and protected.

- State Laws: Each state also has its own laws governing structured settlements, which may vary in specific details. These state laws often complement the SSPA, providing additional protection for recipients and ensuring that the terms of the structured settlement are upheld.

- Regulatory Bodies: In addition to federal and state laws, regulatory bodies, such as state insurance departments, play a role in overseeing structured settlements. These bodies ensure that structured settlement providers are licensed and operate within the bounds of the law. They also investigate complaints related to structured settlements and work to protect consumers from unfair or deceptive practices.

Legal Protections for Recipients

Structured settlements offer significant legal protections for recipients, ensuring that their financial future is secured and that they receive the full benefit of their settlement. These protections include:

- Court Approval: Structured settlements are typically approved by a court, ensuring that the terms of the settlement are fair and equitable. The court reviews the proposed settlement agreement to ensure that it is in the best interests of the recipient, especially in cases involving minors or individuals with disabilities.

- Protection from Assignment: Structured settlements are typically protected from assignment, meaning that the recipient cannot be forced to sell or transfer their rights to the payments. This protection prevents unscrupulous individuals or companies from taking advantage of the recipient’s financial needs.

- Financial Stability: The structured nature of the payments ensures that recipients have a reliable source of income for the long term. This stability protects them from financial hardship and provides peace of mind, knowing that their future is secure.

Requirements and Procedures

Obtaining a structured settlement typically involves a series of steps and procedures, which may vary depending on the specific circumstances of the case. Here are some common requirements and procedures:

- Negotiation: The parties involved in the case, such as the plaintiff and defendant, will negotiate the terms of the settlement, including the amount of the settlement and the structure of the payments.

- Court Approval: The negotiated settlement agreement will typically be submitted to a court for approval. The court will review the agreement to ensure that it is fair and equitable to all parties.

- Structured Settlement Provider: Once the settlement agreement is approved, the parties will work with a structured settlement provider to design and implement the structured settlement. The provider will create a plan for the payments, taking into account the recipient’s needs and financial goals.

Long-Term Planning and Legacy

A structured settlement can be a powerful tool for long-term financial planning and legacy building, ensuring financial security for you and your loved ones for generations to come. It provides a reliable stream of income that can be used to fund future needs and aspirations, safeguarding your family’s financial well-being long after you are gone.

Financial Security for Future Generations

Structured settlements can provide a lasting legacy by ensuring financial security for future generations. The regular payments from a structured settlement can be used to fund a variety of long-term needs, such as:

- Education: Funding college tuition, living expenses, and other educational costs for children and grandchildren.

- Healthcare: Providing financial support for ongoing medical expenses, long-term care, or disability needs.

- Retirement: Supplementing retirement income or creating a secure financial foundation for future generations.

- Business Ventures: Providing capital for starting or expanding businesses, fostering entrepreneurial endeavors.

- Charitable Giving: Establishing a legacy of philanthropy by funding charitable organizations or causes that are important to you.

Examples of Using Structured Settlements for Long-Term Needs

- Funding Education: A structured settlement can be designed to provide regular payments to cover the rising costs of college tuition, books, and living expenses for children and grandchildren, ensuring they have access to quality education. For example, a structured settlement could be set up to provide annual payments of $10,000 for 10 years, totaling $100,000, to cover a child’s college education.

- Healthcare: Structured settlements can provide long-term financial support for medical expenses, particularly for individuals with chronic conditions or disabilities. For instance, a structured settlement could be established to provide monthly payments for ongoing medical treatment, therapy, or home healthcare services, ensuring that individuals have access to the care they need.

- Retirement Planning: Structured settlements can supplement retirement income or create a financial safety net for future generations. By establishing a structured settlement that provides regular payments for a set period, individuals can ensure that their loved ones have a reliable source of income during their retirement years.

Factors to Consider When Choosing a Structured Settlement

The decision to choose a structured settlement over a lump sum payment is a significant one that requires careful consideration of various factors. This section will delve into crucial aspects that individuals should evaluate when making this decision, encompassing financial stability, legal considerations, and personal circumstances.

Financial Stability

Understanding the financial implications of each option is paramount. Structured settlements provide a steady stream of income over time, which can be beneficial for long-term financial planning.

- Predictable Income Stream: Structured settlements offer consistent payments, ensuring a reliable source of income for the recipient. This predictability can be particularly valuable for individuals who require financial stability, such as those with disabilities or long-term medical needs.

- Protection from Financial Mismanagement: By receiving regular payments rather than a lump sum, structured settlements can help mitigate the risk of financial mismanagement or impulsive spending. This can be especially crucial for individuals who may have difficulty managing large sums of money.

- Inflation Protection: Some structured settlements include provisions for inflation adjustments, ensuring that the payments keep pace with the rising cost of living. This can provide valuable protection against the erosion of purchasing power over time.

Legal Considerations

Legal aspects play a crucial role in understanding the nuances of structured settlements. It is essential to consult with legal professionals to ensure a comprehensive understanding of the legal framework surrounding structured settlements.

- Legal and Regulatory Compliance: Structured settlements are subject to specific legal and regulatory requirements. Legal experts can guide individuals through the intricacies of these regulations, ensuring compliance and protecting their rights.

- Contractual Terms and Conditions: The terms and conditions of a structured settlement agreement are legally binding. Legal professionals can review the agreement to ensure that the recipient’s interests are adequately protected.

- Tax Implications: Structured settlements may have different tax implications compared to lump sum payments. Legal and financial advisors can provide guidance on the tax implications of each option.

Personal Circumstances

Personal circumstances, such as age, health, and financial goals, should be carefully considered when deciding between a structured settlement and a lump sum payment.

- Age and Life Expectancy: The duration of the structured settlement payments should align with the recipient’s life expectancy. For individuals with shorter life expectancies, a lump sum payment might be more suitable.

- Health and Medical Needs: Individuals with ongoing medical needs may find the predictable income stream of a structured settlement more advantageous, ensuring consistent funds for healthcare expenses.

- Financial Goals and Lifestyle: Personal financial goals and lifestyle preferences should be factored into the decision. A structured settlement might be preferable for individuals seeking long-term financial security, while a lump sum payment might be more attractive for those with immediate financial needs or investment aspirations.

Seeking Professional Advice

Navigating the complexities of structured settlements requires professional guidance. It is highly recommended to consult with financial advisors and legal experts to obtain personalized advice tailored to individual circumstances.

- Financial Advisors: Financial advisors can assess the recipient’s financial situation, risk tolerance, and long-term goals to determine the most appropriate option. They can also assist with investment planning and wealth management strategies.

- Legal Experts: Legal professionals can provide comprehensive legal guidance on structured settlements, including contractual terms, tax implications, and regulatory compliance. They can also represent the recipient’s interests during negotiations and ensure that the agreement is fair and beneficial.

Ultimately, the decision between a structured settlement and a lump sum is a personal one, best made after careful consideration of your individual circumstances and long-term financial goals. By understanding the benefits of structured settlements, you can make an informed choice that aligns with your financial security and future well-being.

Detailed FAQs

How long do structured settlements last?

The duration of a structured settlement varies depending on the agreement. They can range from a few years to a lifetime, depending on factors such as the severity of the injury and the age of the recipient.

Can I change my mind about a structured settlement after I’ve agreed to it?

While it’s generally difficult to change a structured settlement agreement, there might be circumstances where modifications are possible. It’s essential to consult with legal counsel to understand your options.

Are structured settlements only for personal injury cases?

Structured settlements are commonly used in personal injury cases, but they can also be used in other situations, such as wrongful death settlements or medical malpractice cases.

How do I find a qualified structured settlement expert?

Consult with your attorney, financial advisor, or seek referrals from trusted sources. Look for professionals with experience in structured settlements and a proven track record of success.