A structured settlement offers a stream of payments over time, often stemming from a personal injury or wrongful death case. While this can provide long-term financial security, sometimes circumstances necessitate a lump sum payment. This guide explores the process of selling your structured settlement for immediate cash, including the factors to consider, potential risks, and how to choose a reputable factoring company.

The decision to sell a structured settlement is a complex one. It requires weighing the benefits of a lump sum against the potential downsides of losing future payments. This guide will help you understand the process, navigate the legal complexities, and make an informed decision that aligns with your individual needs and financial goals.

Understanding Structured Settlements

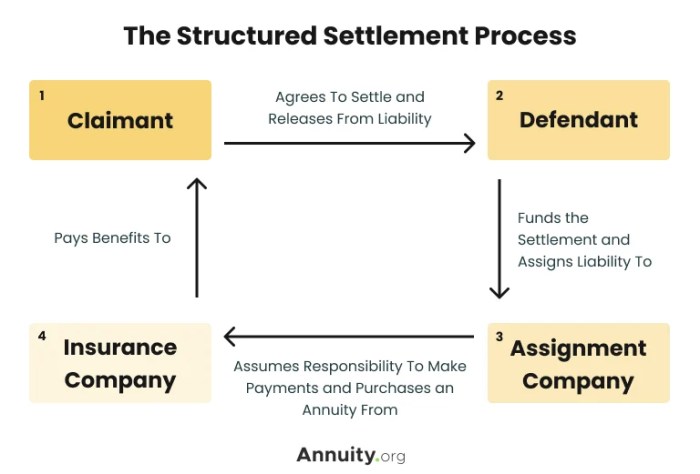

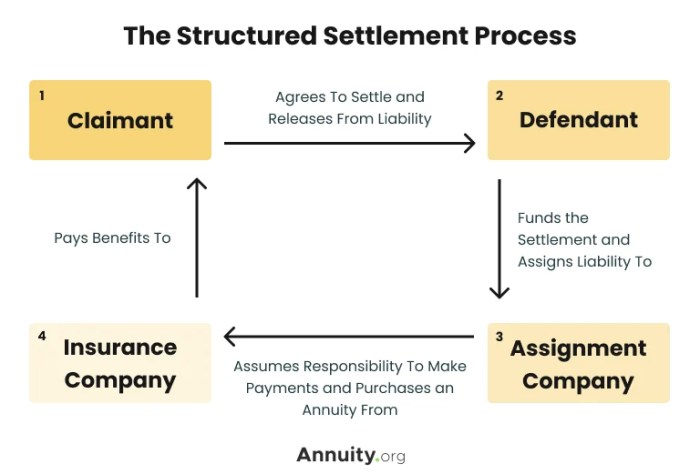

A structured settlement is a legal agreement where a lump-sum payment is divided into a series of periodic payments over time. This arrangement is typically used in personal injury cases, wrongful death cases, or other situations where a person has suffered significant financial losses. Structured settlements are designed to provide long-term financial security for the recipient, ensuring that they have a steady stream of income to cover their needs.

Examples of Structured Settlements

Structured settlements are often used in situations where a person has suffered a severe injury or illness that will impact their ability to work and earn income.

- Personal Injury: In a car accident, a person may receive a structured settlement to cover medical expenses, lost wages, and future care needs.

- Wrongful Death: Families of victims who have died due to negligence or wrongful acts may receive a structured settlement to compensate for their loss.

- Medical Malpractice: If a person has been injured due to medical negligence, a structured settlement can provide long-term financial support for ongoing medical treatment and living expenses.

Benefits of Structured Settlements

Structured settlements offer several advantages for recipients, making them an attractive option in many cases.

- Guaranteed Income Stream: Structured settlements provide a reliable source of income for the recipient, ensuring they have financial stability for the long term.

- Tax Advantages: Payments from a structured settlement are typically tax-free, which can significantly reduce the recipient’s overall tax burden.

- Protection from Financial Mismanagement: By receiving regular payments instead of a lump sum, the recipient is less likely to mismanage or spend the money irresponsibly.

- Professional Management: A structured settlement is often managed by a third-party trustee, ensuring that the funds are invested wisely and distributed according to the terms of the agreement.

Drawbacks of Structured Settlements

While structured settlements offer several benefits, there are also some potential drawbacks to consider.

- Limited Flexibility: The recipient may not be able to access the full value of the settlement at once, which can limit their financial options.

- Inflation: Over time, the value of the payments may be eroded by inflation, making it difficult to maintain the same standard of living.

- Potential for Fraud: There have been instances of fraud related to structured settlements, where unscrupulous individuals attempt to take advantage of recipients.

Reasons for Selling a Structured Settlement

Selling a structured settlement, a series of regular payments received as a result of a legal settlement, can be a complex decision. While structured settlements provide long-term financial security, there are instances where individuals might choose to sell their payments for a lump sum. This decision is often driven by pressing financial needs or personal circumstances.

Financial Hardships and Needs

Many individuals opt to sell their structured settlements due to unforeseen financial difficulties. These hardships might include:

- Medical Expenses: Unanticipated medical bills can create significant financial strain, forcing individuals to seek alternative sources of funding. Selling a structured settlement can provide immediate access to a lump sum payment to cover these expenses.

- Debt Consolidation: High-interest debt, such as credit card debt, can be a significant financial burden. Selling a structured settlement can provide the necessary funds to consolidate debt and reduce monthly payments, leading to improved financial stability.

- Home Repairs or Improvements: Unexpected home repairs or the need for renovations can necessitate a large upfront investment. Selling a structured settlement can provide the required funds to address these needs without incurring substantial debt.

- Education Expenses: Funding higher education for oneself or family members can be a significant financial commitment. Selling a structured settlement can provide the necessary funds to cover tuition, fees, and other educational expenses.

- Business Ventures: Individuals with entrepreneurial aspirations may need a lump sum to start or expand their business. Selling a structured settlement can provide the initial capital to pursue these ventures.

Advantages and Disadvantages

Selling a structured settlement can offer both advantages and disadvantages, which individuals should carefully consider before making a decision.

- Advantages:

- Immediate Access to Funds: Selling a structured settlement provides immediate access to a lump sum payment, which can be used to address urgent financial needs.

- Flexibility and Control: Individuals gain control over their finances by having access to a lump sum, allowing them to allocate funds as needed.

- Potential for Investment: The lump sum received from selling a structured settlement can be invested, potentially generating higher returns than the original structured payments.

- Disadvantages:

- Discount: Structured settlement buyers typically purchase settlements at a discount, meaning individuals will receive less than the total future value of their payments.

- Loss of Future Income: Selling a structured settlement eliminates future payments, potentially impacting long-term financial stability.

- Tax Implications: The lump sum received from selling a structured settlement may be subject to taxes, depending on the specific circumstances.

- Potential for Financial Mismanagement: Individuals who are not financially savvy may mismanage the lump sum received, leading to further financial difficulties.

The Process of Selling a Structured Settlement

Selling a structured settlement involves a series of steps, from contacting a factoring company to receiving your lump sum payment. This process is facilitated by specialized companies known as structured settlement factoring companies.

The Role of Factoring Companies

Factoring companies are financial institutions that purchase structured settlements for a lump sum payment. They assess the value of your settlement, taking into account factors like the remaining payments, interest rates, and your age. Factoring companies play a crucial role in the process by:

- Evaluating your settlement: They analyze the terms of your structured settlement to determine its fair market value.

- Providing a cash offer: They offer you a lump sum payment based on their valuation, which is typically less than the total future value of your settlement.

- Handling the paperwork: They manage all the legal and administrative aspects of transferring your settlement to them.

- Disbursement of funds: Once the transaction is complete, they provide you with your lump sum payment.

Fees and Costs

Selling your structured settlement comes with certain fees and costs. These vary depending on the factoring company and the terms of your settlement. Here’s a breakdown of common fees:

- Factoring fee: This is a percentage of the total settlement amount you receive. It typically ranges from 10% to 30% and is the primary cost associated with selling your structured settlement.

- Legal fees: These are charged by attorneys who handle the legal aspects of the transaction, including drafting and filing the necessary paperwork.

- Other costs: There may be additional fees for things like appraisals, administrative services, or closing costs.

It’s essential to understand that selling your structured settlement will result in a lower overall payout than if you received all the payments as originally scheduled.

Factors Affecting the Value of a Structured Settlement

The value of a structured settlement is determined by several factors that influence the lump sum payment offered. Understanding these factors is crucial for making informed decisions when considering selling your structured settlement.

Factoring companies utilize various methods to calculate the present value of future payments, considering factors like the age of the recipient, the remaining payment term, and the interest rate used for discounting future payments.

Factors Influencing the Lump Sum Payment

The lump sum payment offered for a structured settlement is influenced by various factors, including:

- Remaining Payment Term: The longer the remaining payment term, the higher the present value of the structured settlement. This is because the factoring company needs to compensate for the time value of money, meaning that money received today is worth more than the same amount received in the future.

- Interest Rate: The interest rate used to discount future payments plays a significant role in determining the present value. A higher interest rate will result in a lower present value, while a lower interest rate will result in a higher present value.

- Age of the Recipient: The age of the recipient is a crucial factor, as it influences the remaining payment term and the expected life expectancy. A younger recipient with a longer expected lifespan will generally receive a higher lump sum payment than an older recipient with a shorter expected lifespan.

- Payment Schedule: The frequency and amount of payments also affect the present value. More frequent payments generally result in a higher present value, as the discounting effect is less pronounced.

- State Laws and Regulations: Different states have different laws and regulations governing structured settlements, which can impact the value of the settlement. Some states may have specific requirements for factoring companies or limitations on the amount of money that can be paid for a structured settlement.

- Market Conditions: The overall economic climate and prevailing interest rates can also influence the value of a structured settlement. In a low-interest-rate environment, factoring companies may offer higher lump sum payments to attract sellers.

Methods for Calculating Settlement Value

Factoring companies use various methods to calculate the present value of a structured settlement, including:

- Discounted Cash Flow (DCF) Analysis: This method involves discounting future payments to their present value using a specific discount rate. The discount rate reflects the time value of money and the risk associated with the future payments.

- Internal Rate of Return (IRR) Method: This method calculates the discount rate that makes the present value of the future payments equal to the lump sum payment offered. The IRR represents the return on investment for the factoring company.

- Comparative Market Analysis: This method involves comparing the settlement to similar settlements that have been sold in the past. This helps factoring companies determine a fair market value for the settlement.

Legal Considerations

Selling a structured settlement is a legal transaction with significant implications. It’s essential to understand the legal framework governing these transactions and the potential risks involved. Navigating the legal aspects of selling a structured settlement requires careful consideration and professional guidance.

State Laws and Regulations

State laws regulate structured settlement transactions. Each state has its own set of rules regarding the transfer of structured settlement payments. These laws often require specific disclosures, court approval, and protections for the recipient. For instance, some states require that a court review the transaction to ensure the recipient is not being taken advantage of.

It’s crucial to understand the specific laws in the state where the structured settlement was established.

Potential Risks and Consequences

Selling a structured settlement can have both positive and negative consequences. It’s essential to weigh these factors carefully before making a decision.

- Loss of Future Payments: Selling your structured settlement means giving up the right to receive future payments. This could have a significant impact on your long-term financial security, especially if you need the payments for essential expenses like housing, healthcare, or education.

- Tax Implications: Selling a structured settlement can result in tax consequences. The lump sum payment you receive might be considered taxable income, which could increase your tax liability.

- Fraudulent Transactions: Unfortunately, there have been cases of fraud in the structured settlement industry. Some companies may offer unrealistic or deceptive terms, leaving recipients with less money than they expected.

Alternatives to Selling

Selling your structured settlement may not be the best option for everyone. There are other ways to access your funds that may be more beneficial depending on your individual circumstances.Before you consider selling, it’s crucial to explore these alternatives, which offer flexibility and potentially better financial outcomes.

Borrowing Against Your Structured Settlement

Borrowing against your structured settlement allows you to receive a lump sum payment without permanently relinquishing ownership of your future payments. This option can be advantageous if you need immediate cash but prefer to maintain the long-term financial security of your structured settlement.Here’s how borrowing works:* Lender: You can approach a company specializing in structured settlement loans.

Evaluation

The lender assesses the value of your future payments based on factors like the remaining payment period and interest rates.

Loan Amount

Based on the evaluation, the lender offers you a loan amount, usually a percentage of your structured settlement’s present value.

Repayment

You repay the loan with interest over a predetermined period, often through regular installments deducted from your future structured settlement payments.

Advantages of Borrowing

- Preserves Future Payments: You retain ownership of your structured settlement, ensuring you continue receiving future payments.

- Flexible Repayment: You can tailor the repayment plan to your financial needs, choosing a term that suits your budget.

- Potential Tax Advantages: Depending on your circumstances, interest payments on structured settlement loans may be tax-deductible.

Disadvantages of Borrowing

- Higher Interest Rates: Loan interest rates are typically higher than traditional loans due to the unique nature of structured settlements.

- Reduced Future Payments: Repayments reduce the amount you receive from your future structured settlement payments.

- Potential for Default: Failure to make loan payments can result in default, leading to potential legal consequences and the loss of your structured settlement.

Tips for Choosing a Factoring Company

Finding the right factoring company is crucial to ensure you get the best possible deal for your structured settlement. Several factors come into play when making this decision, and taking the time to carefully evaluate your options will pay off in the long run.

Factors to Consider

When choosing a factoring company, consider the following factors:

- Reputation and Experience: Look for a company with a proven track record of success in the structured settlement factoring industry. Research their history, including customer reviews and industry ratings. Experience in handling structured settlements ensures they understand the complexities involved and can provide accurate valuations.

- Financial Stability: A financially sound company is essential. Check their financial statements, credit rating, and any regulatory approvals to ensure they are stable and reliable.

- Transparency and Communication: Choose a company that is transparent about its fees, processes, and terms. They should be responsive to your questions and concerns, providing clear and concise information throughout the process.

- Valuation Methodology: The company’s valuation method should be fair and accurate. Understand how they determine the value of your structured settlement and compare it to other companies’ methodologies.

- Flexibility and Options: A reputable company will offer flexible payment options and various structuring possibilities to suit your individual needs. Consider whether you prefer a lump sum payment or a series of payments.

- Customer Service: A good factoring company will have excellent customer service. Look for a company with a dedicated team of professionals who are knowledgeable, responsive, and easy to work with.

Research and Comparison

- Online Research: Start your research online by searching for factoring companies specializing in structured settlements. Look for company websites, industry articles, and customer reviews to gather information.

- Industry Associations: Explore reputable industry associations such as the Structured Settlement Trade Association (SSTA) or the National Association of Settlement Purchasers (NASP). These associations can provide information about reputable factoring companies and their standards.

- Compare Quotes: Get quotes from several factoring companies. Ensure you understand their fees, payment terms, and any other conditions before making a decision.

Questions to Ask Potential Factoring Companies

- What is your experience in structured settlement factoring?

- How do you determine the value of a structured settlement?

- What are your fees and payment terms?

- Do you offer any flexible payment options?

- How long does the process take?

- What are the legal implications of selling my structured settlement?

- What are your customer service policies?

Structured Settlements

Structured settlements are a form of compensation often awarded in personal injury or wrongful death cases. They provide regular payments over a set period, offering financial stability and long-term security. This approach contrasts with a lump-sum payment, which provides a single, large sum upfront.

Comparison of Structured Settlements and Lump Sum Payments

The following table highlights the key differences between structured settlements and lump-sum payments:

| Feature | Structured Settlement | Lump Sum Payment |

|---|---|---|

| Payment Structure | Regular payments over time | Single, large payment upfront |

| Financial Security | Provides ongoing income stream | Potential for financial instability if funds are mismanaged |

| Tax Implications | Generally tax-free payments | Taxable income |

| Flexibility | Limited flexibility in accessing funds | High degree of flexibility in using funds |

| Protection from Creditors | Often protected from creditors | Vulnerable to creditor claims |

Key Features and Benefits of Structured Settlements

Structured settlements offer several advantages, including:

| Feature | Benefit |

|---|---|

| Regular Payments | Provides consistent income stream for long-term financial stability |

| Tax-Free Payments | Reduces the tax burden on the recipient |

| Protection from Creditors | Shields funds from creditors, ensuring financial security |

| Professional Management | Ensures responsible management of funds by a third-party trustee |

| Flexibility in Payment Structure | Allows for customization of payment amounts and durations |

Potential Risks and Drawbacks of Structured Settlements

While structured settlements offer benefits, they also come with potential drawbacks:

| Risk | Drawback |

|---|---|

| Limited Access to Funds | Restricted access to funds, making it challenging to meet unexpected expenses |

| Inflation Risk | The purchasing power of future payments may decrease due to inflation |

| Early Termination | The settlement may be terminated prematurely if the recipient dies or becomes disabled |

| Lack of Flexibility | Limited ability to adjust the payment structure after it’s established |

| Potential for Mismanagement | Risk of mismanagement by the trustee, leading to financial losses |

Selling a structured settlement for a lump sum payment can be a viable option when facing immediate financial challenges. By understanding the process, the factors that influence value, and the legal considerations, you can make a well-informed decision that aligns with your specific circumstances. Remember, it’s crucial to work with a reputable factoring company that offers transparency and competitive terms.

Top FAQs

How much can I expect to receive for my structured settlement?

The value of your structured settlement depends on various factors, including the remaining payments, interest rates, and the factoring company’s pricing structure. It’s best to consult with a reputable factoring company for a personalized estimate.

What are the tax implications of selling my structured settlement?

The sale of a structured settlement is generally considered a taxable event. The proceeds received will be subject to income tax, and you may also have to pay capital gains tax. Consult with a tax professional for specific guidance.

Are there any alternatives to selling my structured settlement?

Yes, you can explore options like borrowing against your structured settlement or using it as collateral for a loan. These alternatives might offer more flexibility than selling, but they also come with their own costs and considerations.