Navigating the complexities of personal injury cases often involves making critical decisions about financial compensation. One such decision involves choosing between a lump sum settlement and a structured settlement, which offers a series of regular payments over time. This article delves into the pros and cons of structured settlements, shedding light on their potential benefits and drawbacks for individuals seeking compensation for injuries.

Structured settlements can be particularly beneficial for individuals with long-term medical expenses or who require financial stability over an extended period. The guaranteed payments provide a predictable income stream, mitigating the risk of financial hardship. However, there are also potential drawbacks to consider, such as limited access to the full settlement amount upfront and the possibility of inflation eroding the value of future payments.

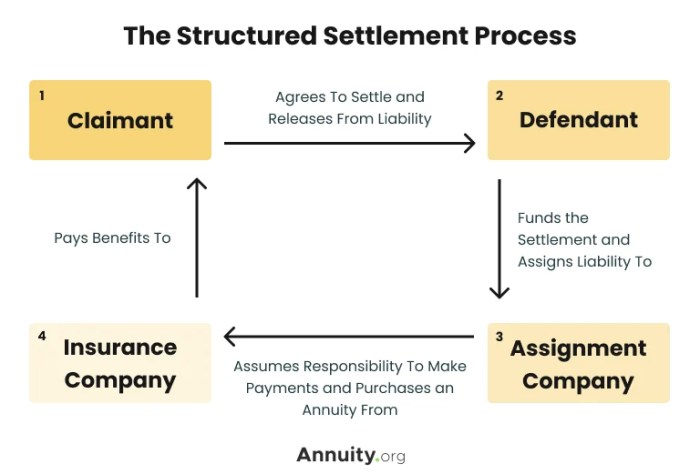

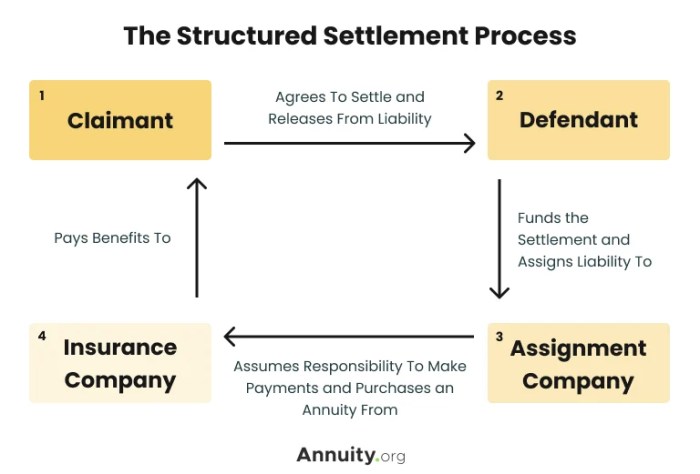

Introduction to Structured Settlements

A structured settlement is a legal agreement that allows a personal injury claimant to receive compensation for their injuries in a series of regular payments over a set period, rather than a single lump sum payment. Structured settlements are often used in cases involving significant injuries, such as brain injuries, spinal cord injuries, or catastrophic illnesses. The purpose of a structured settlement is to provide the claimant with a steady stream of income to cover their ongoing medical expenses, lost wages, and other financial needs.

Rationale for Structured Settlements

Structured settlements offer several benefits for both claimants and defendants:

- Financial Security: Structured settlements provide a predictable source of income for claimants, ensuring they have the financial resources they need to manage their ongoing medical expenses, rehabilitation costs, and other living expenses.

- Protection from Financial Mismanagement: By receiving regular payments instead of a lump sum, claimants are less likely to mismanage their funds, ensuring that the compensation is used for its intended purpose.

- Tax Advantages: Structured settlements often offer tax advantages, as the payments are typically not taxed as ordinary income.

- Reduced Risk for Defendants: Structured settlements can help defendants reduce their financial exposure by spreading out the cost of the settlement over time. This can be particularly beneficial for defendants with limited financial resources.

Common Scenarios for Structured Settlements

Structured settlements are frequently used in a variety of personal injury cases, including:

- Catastrophic Injuries: Cases involving severe injuries such as spinal cord injuries, traumatic brain injuries, or amputations often result in structured settlements due to the high costs associated with long-term medical care and rehabilitation.

- Long-Term Disability: When an individual suffers a permanent disability that prevents them from working, a structured settlement can provide a reliable source of income to cover their living expenses.

- Wrongful Death: In cases where a wrongful death has occurred, a structured settlement can be used to provide financial support to the deceased’s family, including their surviving spouse and children.

Pros of Structured Settlements

Structured settlements offer a unique and often beneficial alternative to lump-sum payments in personal injury cases. They provide a stream of regular payments over a set period, offering financial security and peace of mind for the injured individual.

Guaranteed Payments

Structured settlements provide a guaranteed source of income for the injured individual, ensuring they receive regular payments regardless of their financial situation. This eliminates the risk of mismanaging a lump-sum payment, which can be tempting to spend all at once.

Tax Advantages

Structured settlements often offer tax advantages compared to lump-sum payments. The periodic payments are typically considered tax-free income, while a lump-sum payment may be subject to significant taxes. This can significantly increase the net amount received by the injured individual.

For example, a $1 million lump-sum settlement may be subject to a 20% tax rate, leaving the injured individual with $800,000 after taxes. A structured settlement with the same total value may provide $50,000 per year for 20 years, all tax-free.

Long-Term Financial Security

Structured settlements can provide long-term financial security for injured individuals, ensuring they have a steady stream of income to cover their expenses for years to come. This is particularly important for individuals with long-term disabilities or ongoing medical expenses.

Benefits for Individuals with Ongoing Medical Expenses

Structured settlements are particularly beneficial for individuals with ongoing medical expenses, such as those with chronic injuries or disabilities. The regular payments can be used to cover medical bills, rehabilitation costs, and other expenses related to their injury.

Financial Stability Compared to Lump-Sum Settlements

Structured settlements offer greater financial stability than lump-sum settlements, which can be quickly depleted if not managed wisely. The regular payments ensure that the injured individual has a consistent source of income to cover their needs.

A lump-sum settlement can be easily spent on immediate expenses, leaving the injured individual with little to no money for future needs. Structured settlements provide a steady stream of income, ensuring financial stability for the long term.

Cons of Structured Settlements

Structured settlements, while offering several benefits, also come with certain drawbacks that potential recipients should carefully consider before accepting them. These drawbacks can significantly impact financial planning and overall financial well-being.

Limited Access to Funds

Structured settlements provide a stream of regular payments over a set period. This structure can limit access to a substantial lump sum, which may be desirable for immediate needs or investment opportunities. For instance, individuals requiring significant funds for medical expenses, home renovations, or business ventures might find the structured settlement’s payment schedule insufficient to meet their immediate requirements.

Inflation Risk

Inflation can erode the purchasing power of future payments. Over time, the value of the structured settlement payments may decrease, making it challenging to maintain the same standard of living. For example, a $100,000 structured settlement over 10 years might not have the same purchasing power as a $100,000 lump sum received today due to inflation.

Annuity Provider Failure

Structured settlements rely on annuity providers, which are insurance companies, to make regular payments. If the annuity provider fails financially, there is a risk of losing future payments. While the risk of annuity provider failure is relatively low, it is essential to choose a financially sound and reputable provider.

Impact on Future Financial Planning

Structured settlements can impact future financial planning and investment opportunities. The fixed payment schedule may limit flexibility in managing finances, potentially hindering the ability to take advantage of unexpected opportunities or adjust to changing financial circumstances. For example, an individual with a structured settlement might find it challenging to make significant investments or purchase a new home due to the fixed payment structure.

Flexibility Compared to Lump Sum Settlements

Structured settlements offer less flexibility compared to lump sum settlements. Lump sum settlements provide immediate access to a large sum of money, allowing for greater control and flexibility in financial management. Individuals receiving a lump sum can invest the money, pay off debts, or use it for other purposes as needed.

Factors to Consider When Deciding on a Structured Settlement

Deciding between a structured settlement and a lump sum payment is a significant decision with long-term financial implications. Understanding the factors that influence this choice is crucial to making the best decision for your individual circumstances.

Several factors should be considered when weighing the pros and cons of a structured settlement versus a lump sum payment. These factors include your individual financial needs, your risk tolerance, your ability to manage money, and the potential tax implications of each option. It’s also important to consider the length of time you’ll need financial support and your overall financial goals.

Individual Circumstances and Financial Needs

Your personal financial situation plays a significant role in determining the best settlement option for you. Consider your current financial obligations, such as debt payments, living expenses, and future financial goals, like retirement or education.

- Current Debt Obligations: If you have significant debt, a structured settlement might be more beneficial. It provides a steady stream of income that can be used to pay down debt without risking the entire settlement on a single investment.

- Living Expenses: If you need regular income to cover essential living expenses, a structured settlement can provide a consistent source of funds. A lump sum payment might be tempting but could be quickly depleted without a sound financial plan.

- Future Financial Goals: A structured settlement can help you achieve long-term financial goals, such as saving for retirement or funding a child’s education. The regular payments can be strategically allocated to savings or investments over time.

Risk Tolerance and Ability to Manage Money

Your risk tolerance and ability to manage money are critical factors in determining whether a lump sum payment is suitable for you. A lump sum settlement gives you complete control over your funds, but it also comes with the responsibility of managing them wisely.

- Risk Tolerance: If you are comfortable taking financial risks, a lump sum payment might be appealing. You can invest the funds in higher-yielding assets, potentially generating greater returns. However, it also carries the risk of losing money if investments perform poorly.

- Ability to Manage Money: A lump sum settlement requires strong financial discipline and planning. If you are not confident in your ability to manage large sums of money, a structured settlement might be a safer option. It provides a more predictable income stream, reducing the risk of financial mismanagement.

Tax Implications

The tax implications of a structured settlement and a lump sum payment can vary significantly. It’s essential to consult with a tax professional to understand the potential tax liabilities associated with each option.

- Structured Settlements: Payments from a structured settlement are generally considered tax-free. However, any interest earned on the settlement funds may be subject to taxation.

- Lump Sum Payments: A lump sum payment is generally taxed as ordinary income. The amount of tax you owe will depend on your overall income and tax bracket.

Seeking Legal and Financial Advice

It’s crucial to seek legal and financial advice before making a decision about a structured settlement or a lump sum payment. An attorney can help you understand your legal rights and options, while a financial advisor can help you assess your financial needs and develop a plan for managing your settlement funds.

- Legal Advice: An attorney can review your settlement offer and advise you on the best course of action. They can also help you negotiate with the insurance company to ensure you receive a fair and equitable settlement.

- Financial Advice: A financial advisor can help you develop a budget, manage your investments, and plan for your future financial needs. They can also help you understand the tax implications of each settlement option.

Types of Structured Settlements

Structured settlements offer flexibility in receiving compensation for personal injury cases. They provide a tailored approach to meet individual needs and financial goals, offering a range of payment options beyond a single lump sum.

Types of Structured Settlements

Structured settlements can be categorized into three main types: periodic payments, lump sum payments, and combination settlements. Each type offers distinct benefits and drawbacks, and the most suitable option depends on the specific circumstances of the case.

| Settlement Type | Payment Schedule | Benefits | Drawbacks |

|---|---|---|---|

| Periodic Payments | Regular payments made over a set period, such as monthly, quarterly, or annually. | Provides a steady stream of income for a prolonged period. Can help manage finances and avoid impulsive spending. Potentially tax-advantaged, as payments may be considered tax-free. |

Requires careful planning and budgeting to ensure financial stability. May not provide immediate access to a large sum of money. Potential for inflation to erode the value of future payments. |

| Lump Sum Payments | A single, large payment received at once. | Provides immediate access to a significant amount of money. Allows for flexibility in using the funds for various purposes. |

May lead to financial mismanagement or impulsive spending. Potential for higher taxes on the lump sum amount. May not provide long-term financial security. |

| Combination Settlements | A combination of periodic payments and lump sum payments. | Provides both immediate financial access and long-term income security. Allows for flexibility in meeting both short-term and long-term financial needs. |

Requires careful planning to balance the benefits and drawbacks of both payment types. May be more complex to structure and manage. |

Ultimately, the decision of whether a structured settlement is right for you depends on your individual circumstances and financial needs. Carefully weighing the pros and cons, consulting with legal and financial professionals, and understanding the long-term implications of each option is crucial. By considering all factors involved, individuals can make informed decisions that best suit their unique situations and ensure their financial security in the aftermath of a personal injury.

Clarifying Questions

How long do structured settlement payments last?

The duration of structured settlement payments varies depending on the agreement. They can range from a few years to a lifetime, depending on factors like the severity of the injury and the age of the recipient.

Can I change my mind about a structured settlement after signing the agreement?

Generally, it is difficult to change a structured settlement agreement once it is signed. However, there may be limited circumstances where modifications are possible, such as if the recipient experiences a significant change in their medical condition.

What happens if the annuity provider goes bankrupt?

Structured settlements are typically backed by insurance companies or reputable financial institutions. In the unlikely event of an annuity provider’s bankruptcy, there are mechanisms in place to protect the recipient’s payments, such as state guaranty funds or the possibility of transferring the annuity to another provider.