After a serious injury, navigating the legal and financial landscape can be overwhelming. One crucial decision you’ll face is choosing between a structured settlement and a traditional personal injury lawsuit settlement. While both offer compensation, they differ significantly in how the funds are paid out and the long-term implications. This article explores the advantages and disadvantages of each option, helping you make an informed choice that aligns with your individual needs and goals.

Understanding the nuances of each settlement type is crucial for maximizing your recovery and ensuring financial security. This guide provides a comprehensive overview of structured settlements, personal injury lawsuit settlements, and the key factors to consider when making your decision.

Understanding Structured Settlements

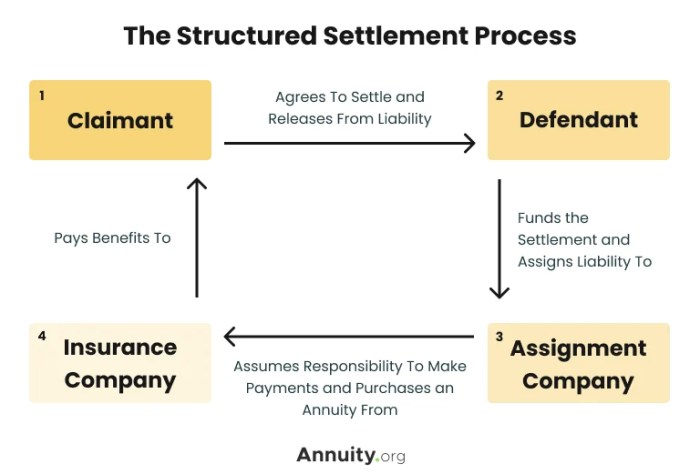

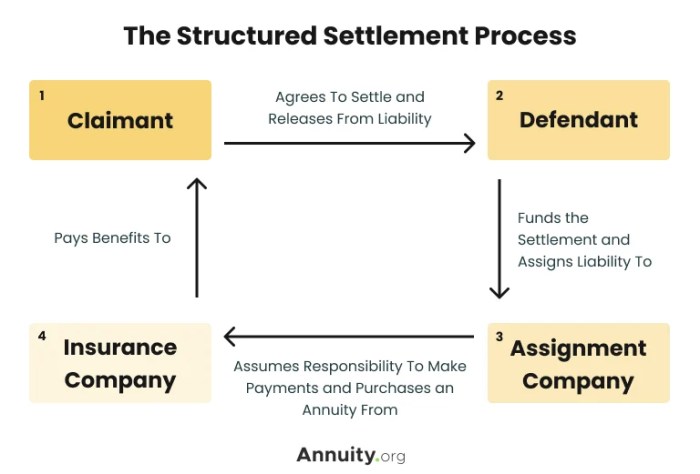

Structured settlements are a unique form of compensation in personal injury cases, offering a structured payment plan instead of a lump sum. They provide a long-term financial solution for victims, ensuring their needs are met over time.

How Structured Settlements Work

Structured settlements are tailored to the specific needs of the injured party. The payments are typically made in regular installments over a set period, often for years or even decades. The amount of each payment and the duration of the settlement are determined by factors such as the severity of the injury, the victim’s age, and their projected future expenses.

Examples of Structured Settlements

- Medical Expenses: Payments can be structured to cover ongoing medical costs, such as rehabilitation, therapy, and medication.

- Lost Wages: Regular installments can compensate for lost income due to the injury, ensuring financial stability during recovery and beyond.

- Future Expenses: Payments can be structured to account for future expenses, such as long-term care or disability accommodations.

Benefits for the Injured Party

- Financial Security: Structured settlements provide a steady stream of income, reducing the risk of financial hardship and ensuring long-term financial stability.

- Protection from Mismanagement: By receiving regular payments, victims are less likely to mismanage funds or make impulsive financial decisions.

- Tax Advantages: In many cases, structured settlements are tax-advantaged, meaning that a portion of the payments may be exempt from taxes.

Benefits for the Defendant

- Cost Control: Structured settlements can be more cost-effective for defendants in the long run, as they spread out the payments over time.

- Reduced Risk: By structuring the payments, defendants reduce the risk of a large lump sum payout that could lead to financial instability for the victim.

- Improved Relationships: Structured settlements can help to build a more positive relationship between the defendant and the injured party, fostering a sense of fairness and resolution.

Personal Injury Lawsuit Settlements

A personal injury lawsuit settlement is a negotiated agreement between a plaintiff and a defendant to resolve a personal injury claim outside of a trial. This agreement involves the defendant paying the plaintiff a specific sum of money in exchange for the plaintiff dropping their lawsuit.

Types of Personal Injury Lawsuit Settlements

There are several types of personal injury lawsuit settlements, each with its own characteristics.

- Lump Sum Settlement: This is the most common type of settlement. The plaintiff receives a single, one-time payment from the defendant.

- Structured Settlement: This settlement involves periodic payments over a set period of time. It is often used in cases with significant damages, ensuring the plaintiff receives financial support over an extended period.

- Contingent Settlement: This settlement is contingent on specific future events, such as the plaintiff’s recovery or the outcome of a medical procedure.

- Mediation Settlement: This settlement is reached through mediation, a process where a neutral third party helps the parties negotiate a resolution.

Factors Influencing the Amount of a Personal Injury Settlement

Several factors can influence the amount of a personal injury settlement. These factors include:

- Nature and Severity of the Injuries: The more severe the injuries, the higher the settlement amount is likely to be. For example, a settlement for a broken bone would likely be lower than a settlement for a spinal cord injury.

- Medical Expenses: The amount of medical expenses incurred due to the injury is a significant factor in determining the settlement amount.

- Lost Wages: The amount of wages lost due to the injury is also considered. This includes past lost wages and potential future lost wages.

- Pain and Suffering: This refers to the physical and emotional distress experienced by the plaintiff due to the injury.

- Liability: The degree to which the defendant is responsible for the injury is a crucial factor. The more liable the defendant is, the higher the settlement amount is likely to be.

- Insurance Coverage: The defendant’s insurance coverage limits can also affect the settlement amount. The insurance company will typically negotiate within the limits of its policy.

- Jurisdiction: Different jurisdictions have different laws regarding personal injury settlements.

- Strength of the Case: The strength of the plaintiff’s case can also influence the settlement amount.

Negotiating a Personal Injury Settlement

Negotiating a personal injury settlement is a complex process that often involves several steps:

- Demand Letter: The plaintiff’s attorney will typically send a demand letter to the defendant outlining the plaintiff’s claims and the amount of compensation sought.

- Settlement Negotiations: The defendant’s insurance company will then respond to the demand letter and engage in negotiations.

- Mediation: If negotiations reach an impasse, mediation may be considered. A neutral third party facilitates communication between the parties to try and reach a settlement.

- Settlement Agreement: If a settlement is reached, it is formalized in a written agreement.

Comparing Structured Settlements and Lawsuit Settlements

Structured settlements and lawsuit settlements are both ways to receive compensation for injuries or damages, but they differ in their structure and how the funds are disbursed. Understanding these differences is crucial for making an informed decision that aligns with your financial needs and long-term goals.

Key Features of Structured Settlements and Lawsuit Settlements

Structured settlements and lawsuit settlements differ in how the compensation is paid out and how the funds are managed.

- Structured settlements involve regular payments over a predetermined period, often monthly or annually. These payments can be adjusted for inflation or other factors.

- Lawsuit settlements typically involve a lump-sum payment, meaning you receive the entire amount of compensation at once.

Advantages and Disadvantages of Structured Settlements

Structured settlements offer several advantages, particularly for those seeking long-term financial security and protection from financial mismanagement.

- Guaranteed income stream: Structured settlements provide a consistent stream of income, ensuring financial stability over time.

- Tax benefits: Payments from structured settlements are often tax-advantaged, with a portion of the payments potentially being tax-free.

- Protection from financial mismanagement: Structured settlements can help prevent the misuse of funds, especially if individuals are prone to impulsive spending or financial hardship.

However, structured settlements also have some drawbacks.

- Lower initial payout: The lump-sum value of a structured settlement is generally lower than the lump-sum value of a lawsuit settlement.

- Limited flexibility: Structured settlements can limit your ability to access the full amount of compensation immediately, potentially hindering large purchases or investments.

- Potential for inflation risk: While some structured settlements account for inflation, others may not, potentially reducing the value of payments over time.

Advantages and Disadvantages of Lawsuit Settlements

Lawsuit settlements offer immediate access to funds, allowing for flexibility in financial planning and decision-making.

- Immediate access to funds: Lawsuit settlements provide a lump-sum payment, giving you full control over the funds right away.

- Greater flexibility: Lawsuit settlements allow you to use the funds for any purpose, including large purchases, investments, or debt repayment.

However, lawsuit settlements also have disadvantages.

- Risk of financial mismanagement: Receiving a large sum of money at once can lead to impulsive spending or poor financial decisions.

- Potential for tax liability: Lawsuit settlements are often subject to taxation, reducing the net amount of compensation received.

- Limited protection from financial hardship: Lawsuit settlements offer no guarantee of financial stability over the long term, leaving you vulnerable to financial hardship.

Comparing Structured Settlements and Lawsuit Settlements

The following table summarizes the key features of structured settlements and lawsuit settlements:

| Feature | Structured Settlements | Lawsuit Settlements |

|---|---|---|

| Payment structure | Regular payments over a predetermined period | Lump-sum payment |

| Tax benefits | Potentially tax-advantaged | Often subject to taxation |

| Financial security | Provides a guaranteed income stream | Limited protection from financial hardship |

| Flexibility | Limited access to funds | Greater control over funds |

| Inflation risk | May not account for inflation | Not affected by inflation |

Choosing the Right Settlement Option

Deciding between a structured settlement and a lump-sum settlement is a significant decision with long-term financial implications. It’s crucial to carefully consider your individual circumstances, financial goals, and risk tolerance to determine the most suitable option.

Factors to Consider When Choosing a Settlement Option

Several factors should be considered when deciding between a structured settlement and a lump-sum settlement. These factors include:

- Financial Goals: Consider your short-term and long-term financial goals. A structured settlement provides a steady stream of income, which can be beneficial for long-term financial security. A lump-sum settlement offers flexibility to invest or spend the money as you see fit.

- Risk Tolerance: A lump-sum settlement allows you to invest the money and potentially grow your wealth, but it also carries the risk of financial loss. A structured settlement eliminates investment risk, but you may miss out on potential investment gains.

- Financial Management Skills: If you lack experience managing large sums of money, a structured settlement may provide greater financial stability.

- Tax Implications: Both structured settlements and lump-sum settlements have tax implications. Consult with a tax advisor to understand the tax consequences of each option.

- Protection from Creditors: Structured settlements are often protected from creditors, which can be a significant advantage for individuals facing financial difficulties.

- Life Expectancy: A structured settlement can be designed to provide income for the rest of your life, which is particularly beneficial if you have a long life expectancy.

Scenarios Where a Structured Settlement May Be More Beneficial

- Individuals with Long-Term Care Needs: A structured settlement can provide a steady stream of income to cover long-term care expenses, such as nursing home costs or home healthcare.

- Individuals with Limited Financial Management Skills: A structured settlement can help individuals who lack financial management skills avoid making risky investments or spending the settlement money unwisely.

- Individuals Facing Financial Difficulties: A structured settlement can provide a reliable source of income, helping individuals manage their debts and avoid financial instability.

- Individuals with a Long Life Expectancy: A structured settlement can ensure a steady stream of income for the rest of their lives, providing financial security throughout their retirement years.

Scenarios Where a Lump-Sum Settlement Might Be Preferable

- Individuals with Specific Financial Goals: If you have a specific financial goal in mind, such as purchasing a home, starting a business, or paying off debt, a lump-sum settlement may provide the necessary funds to achieve those goals.

- Individuals with Strong Investment Skills: If you have a strong understanding of financial markets and are comfortable taking investment risks, a lump-sum settlement may allow you to grow your wealth significantly.

- Individuals with a Short Life Expectancy: If you have a shorter life expectancy, a lump-sum settlement may be more beneficial, as you will have less time to benefit from a structured settlement.

Structured Settlements and Financial Planning

Structured settlements can play a crucial role in your financial planning, especially after a life-altering event like a personal injury. They provide a consistent stream of income that can be incorporated into your long-term financial strategies.

By understanding how structured settlements work, you can make informed decisions about managing these funds and achieving your financial goals.

Tax Implications of Structured Settlements

Understanding the tax implications of structured settlements is crucial for effective financial planning. The tax treatment of structured settlements depends on the nature of the underlying claim and the specific terms of the settlement agreement. Here’s a breakdown of the potential tax implications:

| Type of Settlement | Taxability |

|---|---|

| Personal Injury Settlements | Generally, payments received from personal injury settlements are tax-free. This includes compensation for physical pain and suffering, emotional distress, and medical expenses. However, punitive damages, which are intended to punish the wrongdoer, are typically taxable. |

| Wrongful Death Settlements | Payments received from wrongful death settlements are generally tax-free. However, interest earned on the settlement proceeds may be taxable. |

| Other Settlements (e.g., property damage) | Payments received from settlements for property damage or other non-personal injury claims are typically taxable as ordinary income. |

Managing Structured Settlement Funds

Managing structured settlement funds requires careful planning and consideration. Here are some tips to ensure your funds are used effectively and meet your long-term financial goals:

- Create a Budget: Developing a detailed budget is essential for tracking your income and expenses. This will help you understand how much you can allocate towards different financial goals.

- Establish Financial Goals: Define your financial objectives, such as saving for retirement, paying off debt, or funding education. This will guide your investment and spending decisions.

- Seek Professional Advice: Consult with a financial advisor to discuss your specific financial situation and create a personalized plan for managing your structured settlement funds.

- Consider Investing: Investing your structured settlement funds can help them grow over time. A financial advisor can assist you in choosing appropriate investments based on your risk tolerance and time horizon.

- Protect Your Funds: Be aware of potential scams and fraudulent schemes targeting structured settlement recipients. Only work with reputable financial professionals and organizations.

Ultimately, the choice between a structured settlement and a lump-sum settlement depends on your individual circumstances, financial goals, and risk tolerance. By carefully weighing the pros and cons of each option, you can make an informed decision that sets you on the path to a successful recovery and financial stability.

Answers to Common Questions

What is a structured settlement?

A structured settlement is a legal agreement that provides periodic payments to an injured party over a set period. These payments are typically tax-free and can be used to cover medical expenses, lost wages, and other damages.

What is a lump-sum settlement?

A lump-sum settlement is a single, one-time payment made to the injured party. This payment can be used for any purpose, but it is subject to taxes.

What are the advantages of a structured settlement?

Structured settlements provide a steady stream of income, which can help with long-term financial planning. They are also generally tax-free, which can save you money in the long run.

What are the disadvantages of a structured settlement?

Structured settlements can be difficult to manage, as you will need to track your payments and make sure they are used wisely. You also may not have access to the full amount of your settlement immediately.

What are the advantages of a lump-sum settlement?

A lump-sum settlement gives you immediate access to a large amount of money, which can be used to pay off debts, invest, or purchase a home.

What are the disadvantages of a lump-sum settlement?

Lump-sum settlements are subject to taxes, which can significantly reduce the amount of money you receive. You also may be tempted to spend the money unwisely, which could lead to financial problems in the future.