Receiving a structured settlement can be a complex process, especially when it comes to understanding the tax implications. While structured settlements offer a unique way to manage funds over time, navigating the intricacies of tax treatment can be challenging. This guide delves into the various tax implications of receiving structured settlement payments, providing a comprehensive overview for individuals seeking clarity on this important topic.

Structured settlements are often used in personal injury cases, medical malpractice claims, or wrongful death lawsuits. They provide a stream of regular payments over a set period, rather than a single lump sum. This approach can offer several benefits, including financial stability and tax advantages, but it’s crucial to understand the potential tax implications to ensure you’re maximizing your financial outcome.

Understanding Structured Settlements

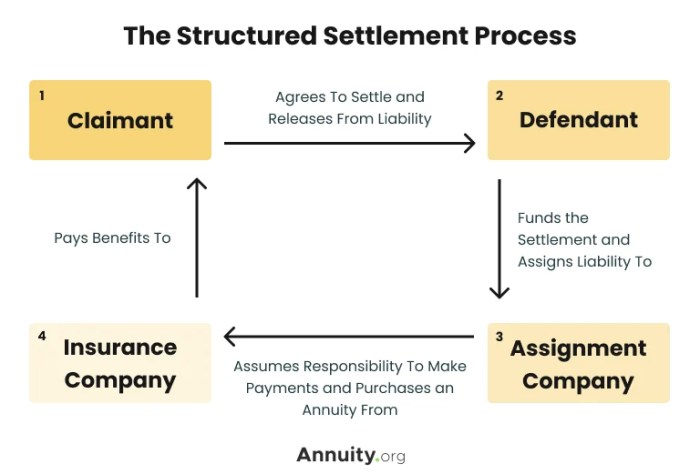

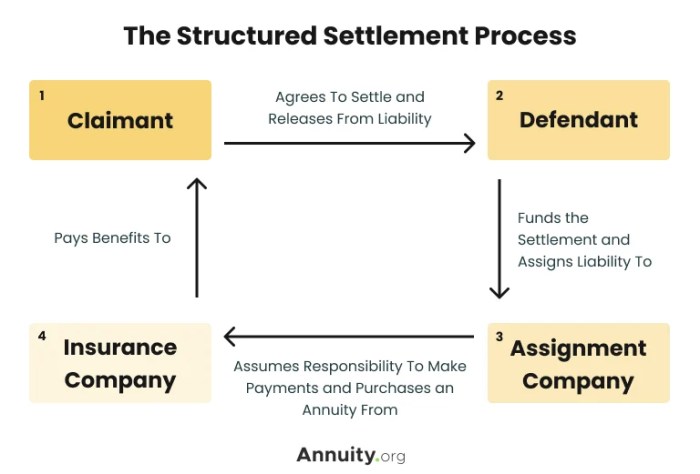

A structured settlement is a legal agreement that allows a person who has received a personal injury settlement to receive their funds in regular payments over a period of time, rather than in a lump sum. This type of settlement is often used in cases where the injured party has significant medical expenses or ongoing needs.Structured settlements are designed to provide a steady stream of income for the injured party, helping them manage their finances and avoid the risk of spending the entire settlement amount quickly.

They can also be helpful in protecting the funds from creditors or mismanagement.

Examples of Structured Settlements

Structured settlements are commonly used in a variety of situations, including:

- Personal injury cases: This is the most common use of structured settlements. For example, a person who has been seriously injured in a car accident may receive a structured settlement to cover their medical expenses, lost wages, and pain and suffering.

- Wrongful death cases: When a family member dies as a result of someone else’s negligence, the family may receive a structured settlement to provide for their financial needs.

- Medical malpractice cases: If a patient is injured due to a doctor’s negligence, they may receive a structured settlement to cover their medical expenses, lost wages, and pain and suffering.

Benefits and Drawbacks of Structured Settlements

Structured settlements offer several potential benefits over lump-sum payments, but they also have some drawbacks.

Benefits

- Financial security: Structured settlements provide a steady stream of income, helping the injured party manage their finances and avoid the risk of spending the entire settlement amount quickly.

- Protection from creditors: The payments from a structured settlement are generally protected from creditors, meaning that they cannot be seized to pay off debts.

- Tax advantages: In some cases, the payments from a structured settlement may be tax-free or partially tax-free.

- Professional management: A structured settlement is managed by a third party, such as an insurance company or a trust, which can help ensure that the funds are used wisely.

Drawbacks

- Loss of control: With a structured settlement, the injured party does not have direct control over the funds. They receive payments according to the terms of the agreement, and they cannot access the entire settlement amount at once.

- Limited flexibility: The terms of a structured settlement are fixed, and the injured party may not be able to change the payment schedule or the amount of the payments.

- Potential for inflation: The value of the payments from a structured settlement may be eroded by inflation over time.

Tax Implications of Structured Settlement Payments

Structured settlements, which are often used in personal injury cases, can provide a stream of income over a period of time. However, understanding the tax implications of these payments is crucial for both the recipient and the payer.

Tax Treatment of Structured Settlement Payments

The tax treatment of structured settlement payments depends on the nature of the underlying claim. Payments received for physical injuries or sickness are generally considered tax-free, while payments for lost wages or other economic damages are typically taxable.

- Payments for physical injuries or sickness: These payments are generally considered tax-free because they are intended to compensate for the pain and suffering caused by the injury or sickness. Examples include payments for medical expenses, lost wages due to disability, and pain and suffering.

- Payments for lost wages or other economic damages: These payments are generally considered taxable because they are intended to compensate for the financial losses incurred due to the injury or sickness. Examples include payments for lost wages due to lost work opportunities and lost earning capacity.

Difference in Tax Implications Between Periodic Payments and Lump-Sum Payments

The tax treatment of structured settlement payments can also vary depending on whether the payments are made periodically or in a lump sum.

- Periodic Payments: Periodic payments are typically made in installments over a period of time. These payments are generally taxed as ordinary income in the year they are received.

- Lump-Sum Payments: Lump-sum payments are made in a single payment. These payments are generally taxed as ordinary income in the year they are received, but they may also be subject to a penalty if they are withdrawn early from a structured settlement annuity.

Examples of Tax Treatment Under Various Laws and Regulations

Here are some examples of how structured settlements are treated under various tax laws and regulations:

- Internal Revenue Code Section 104(a)(2): This section of the Internal Revenue Code exempts from taxation payments received for personal injuries or sickness.

- Internal Revenue Code Section 104(a)(3): This section of the Internal Revenue Code exempts from taxation payments received for lost wages due to disability.

- Internal Revenue Code Section 72: This section of the Internal Revenue Code governs the taxation of annuity payments, including structured settlement payments.

It is important to note that the tax treatment of structured settlement payments can be complex and vary depending on the specific circumstances. It is always advisable to consult with a tax professional to determine the tax implications of a particular structured settlement.

Taxable Income from Structured Settlements

Structured settlements are generally not subject to federal income tax, but there are some exceptions. Income from structured settlements can be taxed if it represents interest or if the settlement is structured in a way that creates taxable income.

Interest Payments

Interest payments included in structured settlement payments are generally considered taxable income. The IRS considers these payments as interest income, which is subject to taxation. The amount of interest included in each payment is usually specified in the settlement agreement.

For example, if a structured settlement payment includes $10,000 in principal and $500 in interest, the $500 in interest would be considered taxable income.

Taxable Income from Structured Settlements

Here are some situations where structured settlements can generate taxable income:

- Structured settlements that include interest payments: As discussed above, interest payments are generally considered taxable income. The IRS considers these payments as interest income, which is subject to taxation.

- Structured settlements that are structured as annuities: If a structured settlement is structured as an annuity, the payments may be subject to tax depending on the type of annuity. For example, if the structured settlement is a fixed annuity, the payments may be subject to ordinary income tax. However, if the structured settlement is a variable annuity, the payments may be subject to capital gains tax.

- Structured settlements that are structured as trusts: If a structured settlement is structured as a trust, the income from the trust may be subject to tax. The tax implications of a trust depend on the specific terms of the trust agreement.

- Structured settlements that are used to purchase an asset: If a structured settlement is used to purchase an asset, the gain on the sale of the asset may be subject to tax. For example, if a structured settlement is used to purchase a house, the gain on the sale of the house may be subject to capital gains tax.

Deductible Expenses Related to Structured Settlements

It’s important to understand that certain expenses related to structured settlements may be deductible. These deductions can help reduce your overall tax liability and potentially save you money. Expenses related to structured settlements can be deductible if they meet certain criteria, such as being ordinary and necessary, directly related to the settlement, and properly documented.

Deductible Expenses

The deductibility of expenses related to structured settlements can be complex. Here are some common expenses that may be deductible:

- Legal Fees: Legal fees incurred in negotiating and obtaining the structured settlement are often deductible. This includes fees paid to attorneys who helped you secure the settlement.

- Expert Witness Fees: Fees paid to experts who provide testimony or evidence in support of your claim can also be deductible. This may include medical experts, financial experts, or other professionals.

- Court Costs: Expenses associated with court proceedings, such as filing fees, service fees, and other court-related costs, may be deductible.

- Medical Expenses: If the structured settlement is related to a personal injury or illness, you may be able to deduct certain medical expenses, such as doctor’s visits, hospital stays, and prescription drugs.

Criteria for Deductible Expenses

To be deductible, expenses related to structured settlements must meet the following criteria:

- Ordinary and Necessary: The expenses must be considered ordinary and necessary in the context of obtaining and managing the structured settlement.

- Directly Related: The expenses must be directly related to the structured settlement. This means the expenses must have been incurred specifically for the purpose of obtaining or managing the settlement.

- Properly Documented: You must have proper documentation to support your deductions. This includes receipts, invoices, and other records that clearly show the nature and amount of the expenses.

It’s important to consult with a tax professional to determine which expenses are deductible in your specific situation.

Reporting Structured Settlement Payments on Tax Returns

Structured settlement payments are generally considered taxable income. However, the specific tax implications depend on the type of settlement and the terms of the agreement. It’s crucial to understand how to report these payments accurately on your tax return to avoid any penalties.

Reporting Structured Settlement Payments on Tax Returns

When reporting structured settlement payments on your tax returns, it’s essential to follow the specific instructions provided by the IRS. These instructions vary depending on the type of settlement and the tax year in question.

Step-by-Step Guide for Reporting Structured Settlement Payments

- Identify the type of structured settlement: Determine whether the structured settlement is for personal injury, property damage, or other reasons. This will help you understand the specific tax implications of the payment.

- Determine the taxable portion of the payment: Generally, structured settlement payments are considered taxable income. However, some portions may be exempt from taxes, such as payments for medical expenses or lost wages. Consult with a tax professional to determine the taxable portion of your settlement.

- Gather necessary documentation: Collect all relevant documentation related to your structured settlement, including the settlement agreement, payment schedule, and any tax forms received from the payer.

- Report the payment on your tax return: Use the appropriate IRS forms and sections to report the structured settlement payments. This will typically involve reporting the payments as ordinary income on your Form 1040.

- Maintain accurate records: Keep detailed records of all structured settlement payments, including the date of receipt, the amount received, and the source of the payment. This will help you accurately report the payments on your tax return and ensure you are in compliance with tax laws.

Forms and Sections for Reporting Structured Settlements

| Form | Section | Description |

|---|---|---|

| Form 1040 | Line 21 | Report all taxable income, including structured settlement payments |

| Schedule A (Itemized Deductions) | Various | Report deductible expenses related to the structured settlement, such as medical expenses or legal fees |

| Form 1099-R | Various | Received from the payer of the structured settlement, reporting the amount of the payment and any applicable tax withholdings |

Considerations for Tax Planning with Structured Settlements

Structured settlements offer a unique way to manage financial resources following a significant event, but understanding their tax implications is crucial for effective planning. This section explores key factors to consider, strategies for minimizing tax liability, and the importance of seeking professional guidance.

Factors to Consider When Planning for Tax Implications

Understanding the tax implications of structured settlements requires careful consideration of various factors. These include:

- Type of Settlement: The nature of the settlement, such as personal injury, wrongful death, or property damage, can influence taxability.

- State Laws: Tax rules can vary from state to state, so understanding your state’s regulations is essential.

- Federal Laws: The Internal Revenue Code Artikels specific rules regarding structured settlements. Staying updated on these regulations is vital.

- Investment Options: How the settlement funds are invested can affect tax consequences, particularly in terms of capital gains or losses.

- Future Income: Anticipating future income from the settlement, including interest payments and potential growth, is crucial for long-term tax planning.

Strategies for Minimizing Tax Liability

Several strategies can help minimize the tax liability associated with structured settlements.

- Structured Settlement Factoring: Selling a portion of your settlement to a third party can generate immediate cash while potentially reducing future tax obligations. However, this option requires careful consideration of its implications and potential drawbacks.

- Tax-Advantaged Investments: Investing settlement funds in tax-advantaged accounts like 401(k)s or IRAs can defer tax payments until retirement. However, withdrawal rules and tax implications during retirement should be understood.

- Charitable Donations: Donating a portion of the settlement to qualified charities can reduce your taxable income, but specific rules and regulations apply. Consulting a tax advisor is recommended.

- Tax Planning with Professional Guidance: Seeking professional tax advice from a qualified accountant or financial advisor can help you develop a personalized plan to minimize tax liability and optimize your financial well-being.

Seeking Professional Guidance

Given the complexities of tax laws and the unique nature of structured settlements, it’s highly recommended to consult with a qualified tax professional. A professional can:

- Analyze Your Specific Situation: A tax professional can assess your individual circumstances, including the type of settlement, state of residence, and investment goals.

- Develop a Personalized Plan: Based on your needs, a professional can create a customized tax plan that minimizes your tax liability and optimizes your financial strategy.

- Stay Updated on Tax Laws: Tax laws are subject to change, and a professional can keep you informed about the latest regulations and their impact on your settlement.

Comparing Tax Implications of Structured Settlements with Other Settlement Options

Understanding the tax implications of different settlement options is crucial for maximizing your financial benefits. While structured settlements offer tax advantages, it’s essential to compare them with lump-sum payments to determine the most advantageous approach for your situation.

Tax Treatment of Lump-Sum Payments

Lump-sum payments are generally taxed as ordinary income, meaning they are subject to your regular income tax rates. This can result in a significant tax liability, especially if the settlement amount is substantial. However, certain exceptions exist, such as payments for physical injuries or sickness, which may be excluded from taxable income.

Advantages and Disadvantages of Structured Settlements vs. Lump-Sum Payments

- Structured Settlements:

- Advantages:

- Tax-advantaged treatment: Portions of structured settlement payments are often tax-free, as they are considered “damages” for physical injuries or sickness.

- Financial security: Regular payments provide a predictable income stream, ensuring financial stability over time.

- Protection from financial mismanagement: Structured settlements prevent you from spending the entire settlement amount at once, mitigating the risk of financial mismanagement.

- Disadvantages:

- Lower immediate cash flow: You receive smaller payments over time, which may not be ideal for immediate needs.

- Potential for inflation: The value of future payments may be eroded by inflation.

- Limited flexibility: Structured settlements may not be as flexible as lump-sum payments, as you may not be able to access the entire settlement amount at once.

- Lump-Sum Payments:

- Advantages:

- Immediate access to funds: You have immediate control over the entire settlement amount, allowing for greater flexibility and investment opportunities.

- Potential for higher investment returns: You can invest the lump-sum payment and potentially earn higher returns than the interest rates on structured settlement payments.

- Disadvantages:

- Higher tax liability: Lump-sum payments are generally taxed as ordinary income, resulting in a significant tax burden.

- Risk of financial mismanagement: The potential for mismanaging a large sum of money can lead to financial instability.

- Limited long-term financial security: A lump-sum payment may not provide a steady income stream for the long term, potentially leading to financial challenges later on.

Comparison Table: Tax Treatment of Settlement Options

| Settlement Option | Tax Treatment | Advantages | Disadvantages |

|---|---|---|---|

| Structured Settlement | Portions may be tax-free, depending on the nature of the claim. | Tax-advantaged treatment, financial security, protection from mismanagement. | Lower immediate cash flow, potential for inflation, limited flexibility. |

| Lump-Sum Payment | Generally taxed as ordinary income. | Immediate access to funds, potential for higher investment returns. | Higher tax liability, risk of financial mismanagement, limited long-term financial security. |

Navigating the tax implications of structured settlements requires careful consideration and planning. Understanding the tax treatment of different aspects of your settlement, including interest payments and deductible expenses, can significantly impact your overall financial outcome. Consulting with a tax professional is highly recommended to ensure you are maximizing your benefits and minimizing your tax liability. By gaining a comprehensive understanding of the tax implications, you can make informed decisions about your structured settlement and ensure your financial well-being.

FAQ Insights

How are structured settlement payments taxed?

The tax treatment of structured settlement payments depends on the source of the settlement. Payments received for physical injuries or sickness are generally considered non-taxable, while payments for lost wages or other economic damages are usually taxable as ordinary income.

What if my structured settlement includes interest payments?

Interest payments included in structured settlement payments are generally taxable as ordinary income. The amount of interest will be reported on Form 1099-INT, and you will need to include it in your taxable income.

Can I deduct any expenses related to my structured settlement?

You may be able to deduct certain expenses related to your structured settlement, such as legal fees or medical expenses. The deductibility of these expenses will depend on your specific circumstances and the applicable tax laws.

How do I report my structured settlement payments on my tax return?

You will need to report your structured settlement payments on your tax return using Form 1040. The specific forms and sections used will depend on the type of income received and any deductible expenses.